Get a Blank W-4

1:35

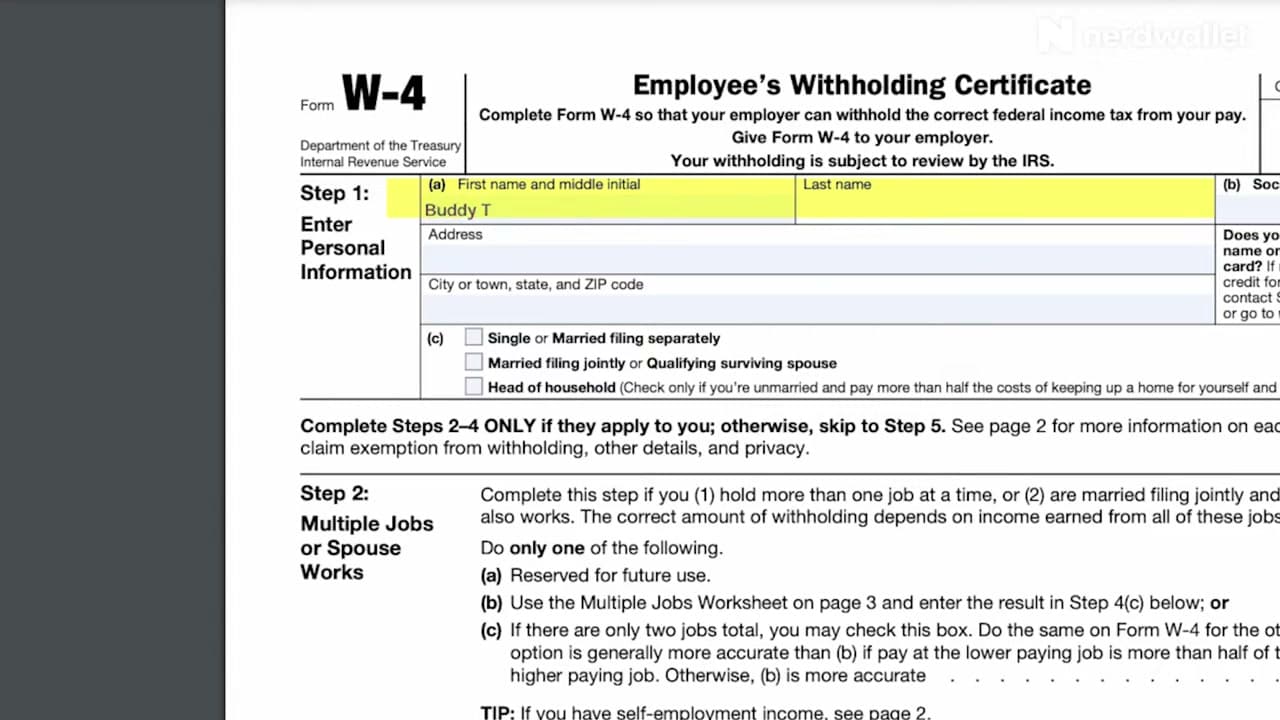

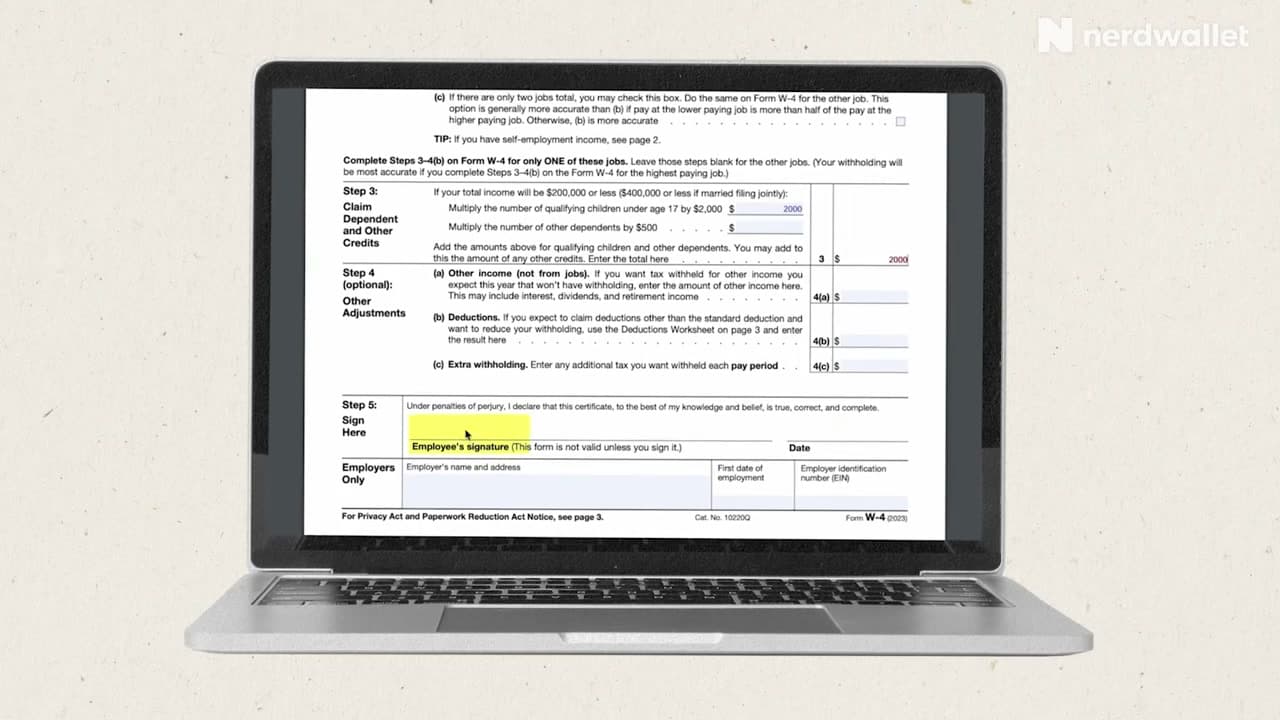

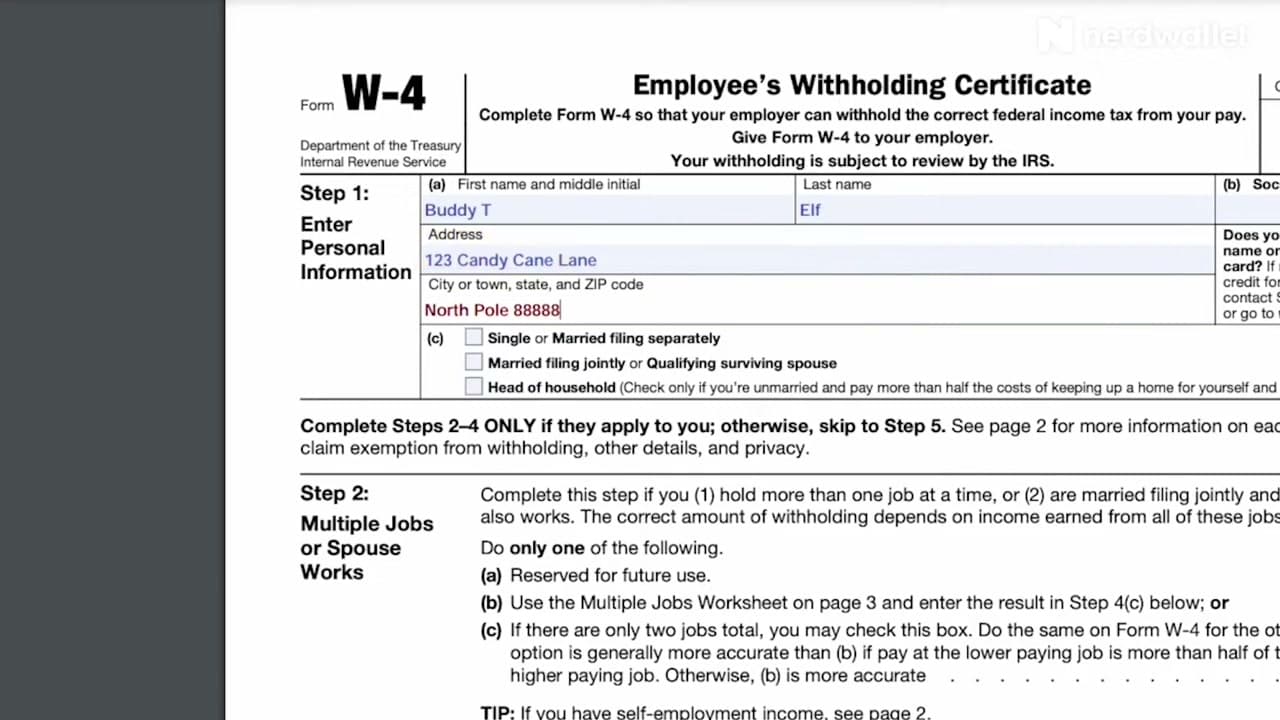

Your employer almost always hands you a blank W-4 during new-hire paperwork. If you misplaced it or need to update an old one, download the current version from the IRS at irs.gov/forms-pubs/about-form-w-4. Make sure it says "Form W-4" across the top and that it's the current tax year.

The W-4 is not the same as the W-2. The W-4 tells your employer how much to withhold from each paycheck. The W-2 is the year-end summary you get in January. Keep a pen handy and have your Social Security card and most recent tax return nearby - you'll reference both.

Tip

If you're a contractor or freelancer rather than a W-2 employee, you'll get a W-9 instead. The W-9 is much shorter and only collects your taxpayer ID so the company can send you a 1099 at year end.