1

What a 401(k) Actually Is

0:42

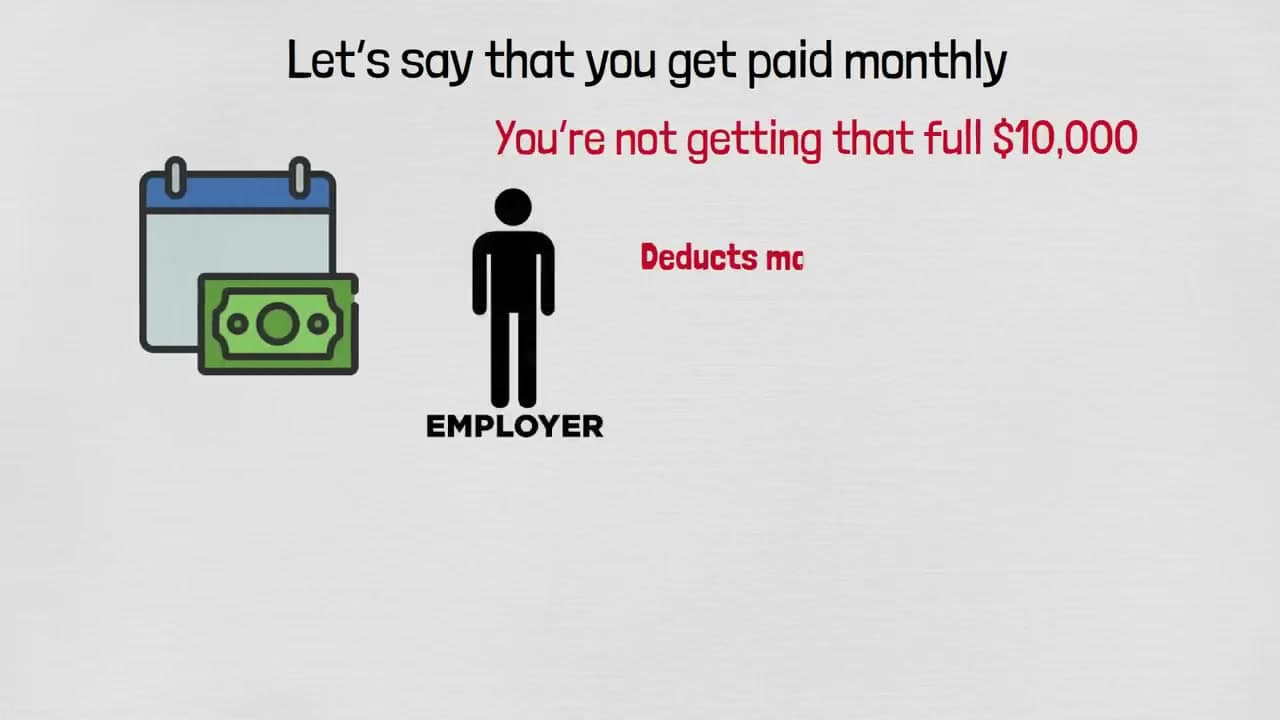

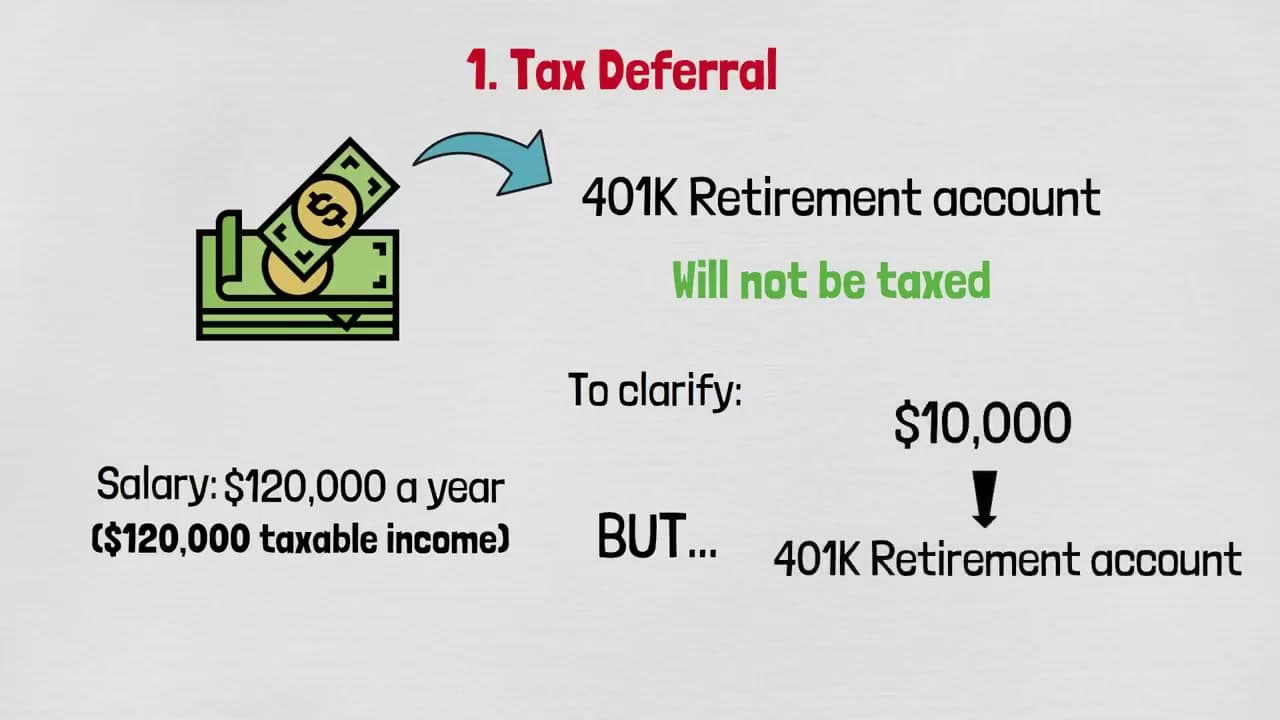

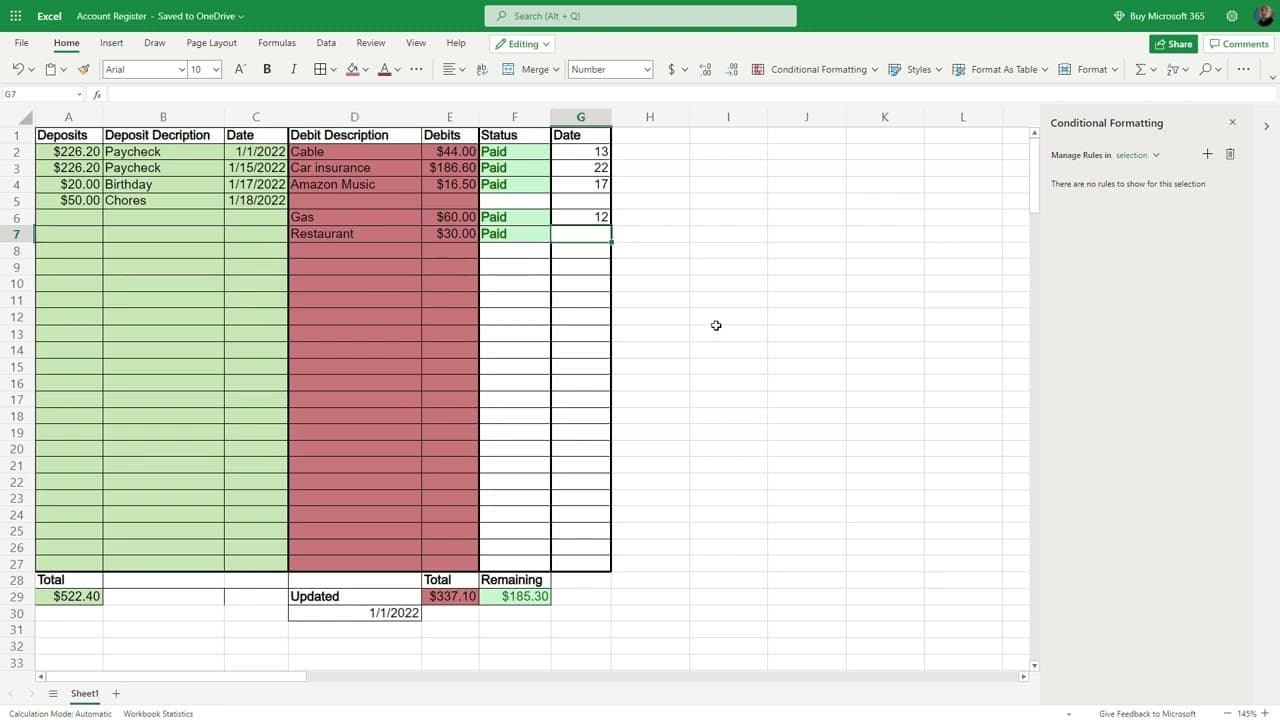

A 401(k) is a retirement savings account your employer offers. You pick a percentage of each paycheck to put in, and that money goes directly into the account before taxes are calculated. You never see it in your take-home pay.

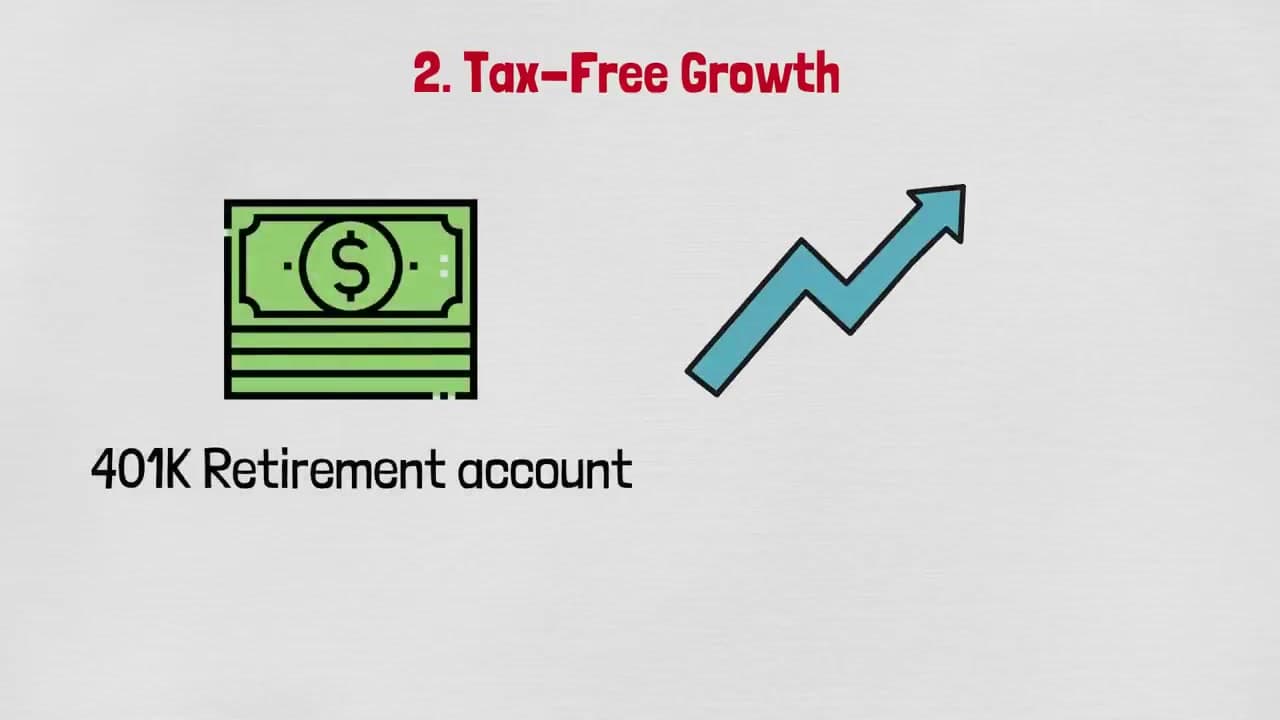

Inside the account, your money gets invested — stocks, bonds, mutual funds — depending on what options your employer's plan includes. The account is in your name, and the balance is yours to keep.

Tip

If your employer offers a 401(k) and you're not sure whether you're enrolled, check your most recent pay stub — 401(k) contributions usually show up as a line item deduction.