Step 1: Know the 300-to-850 Scale

0:04

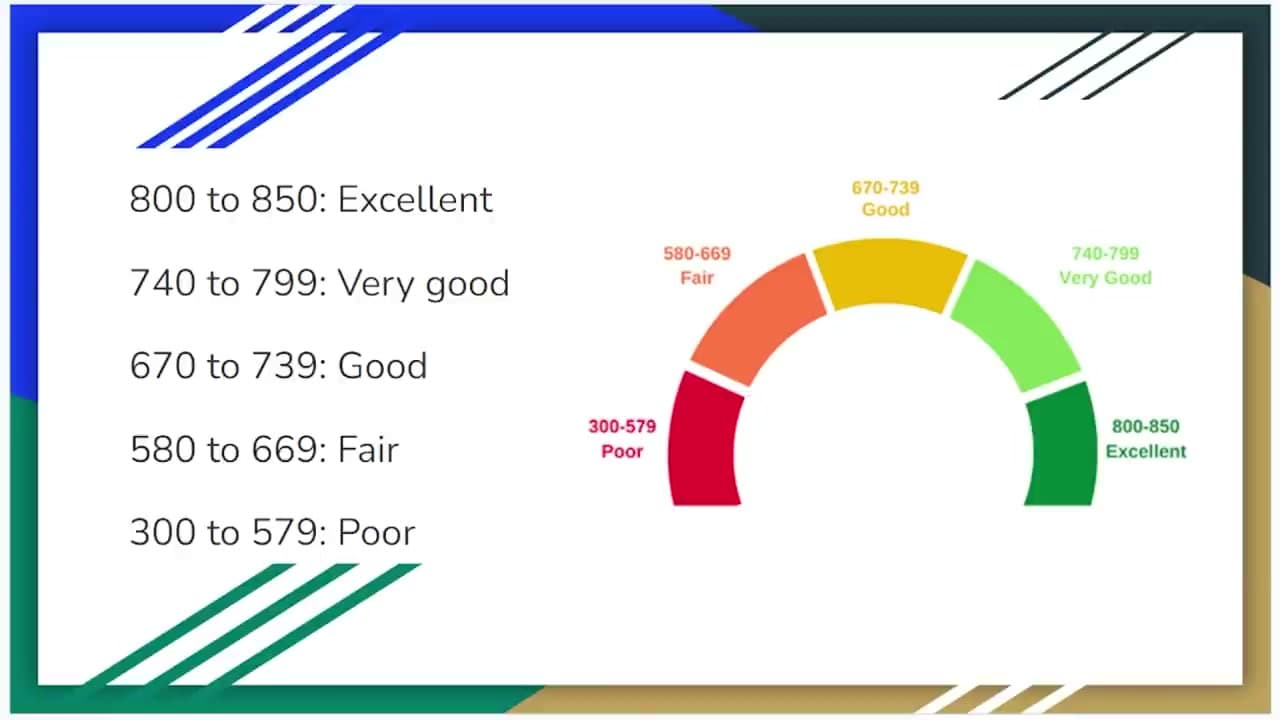

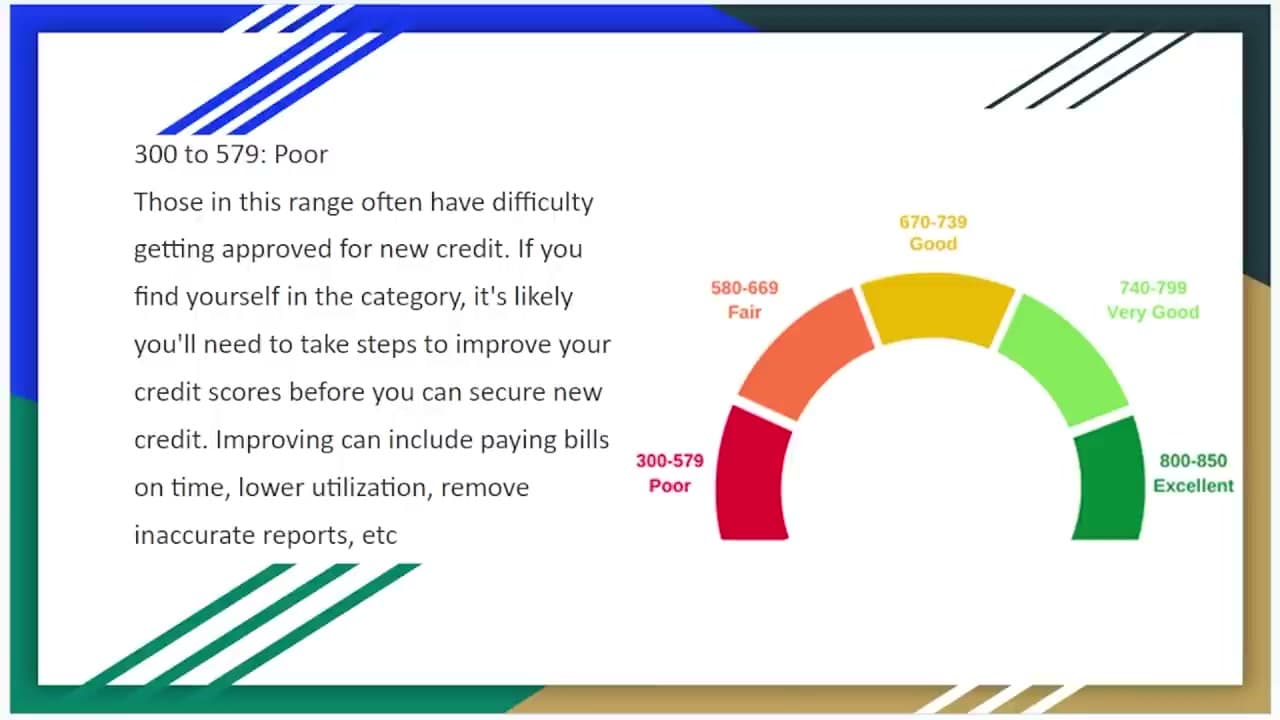

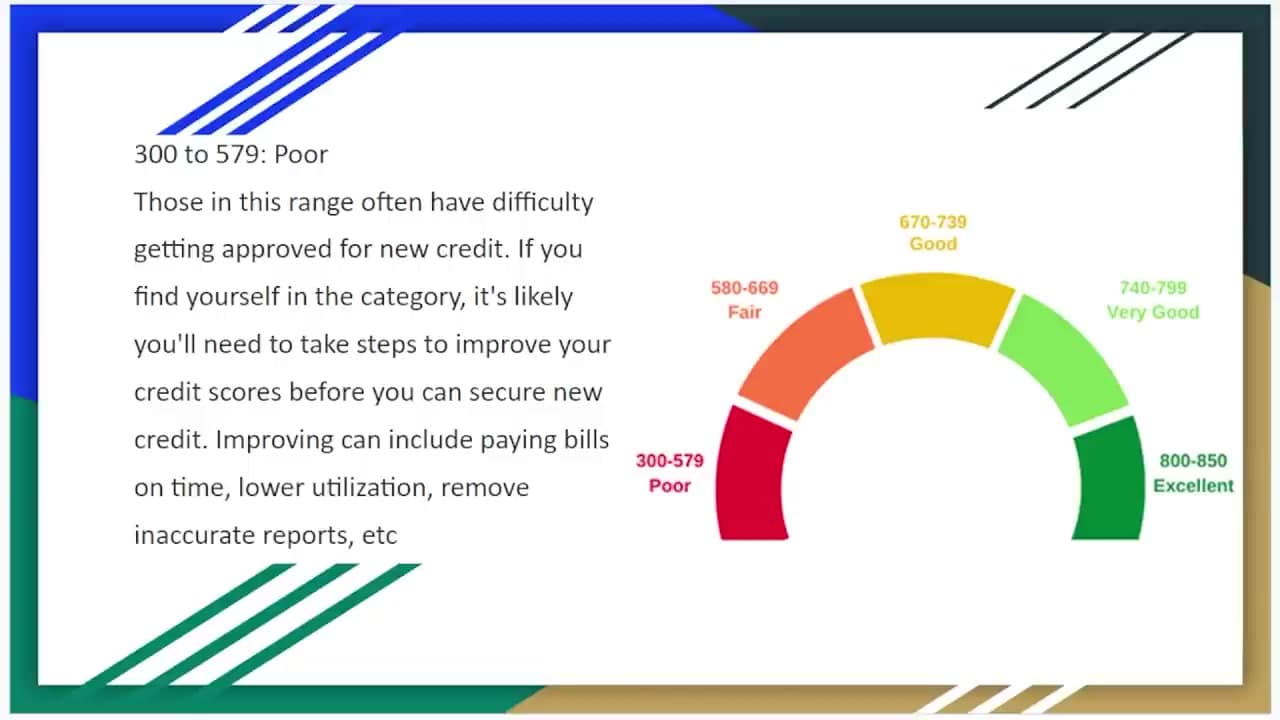

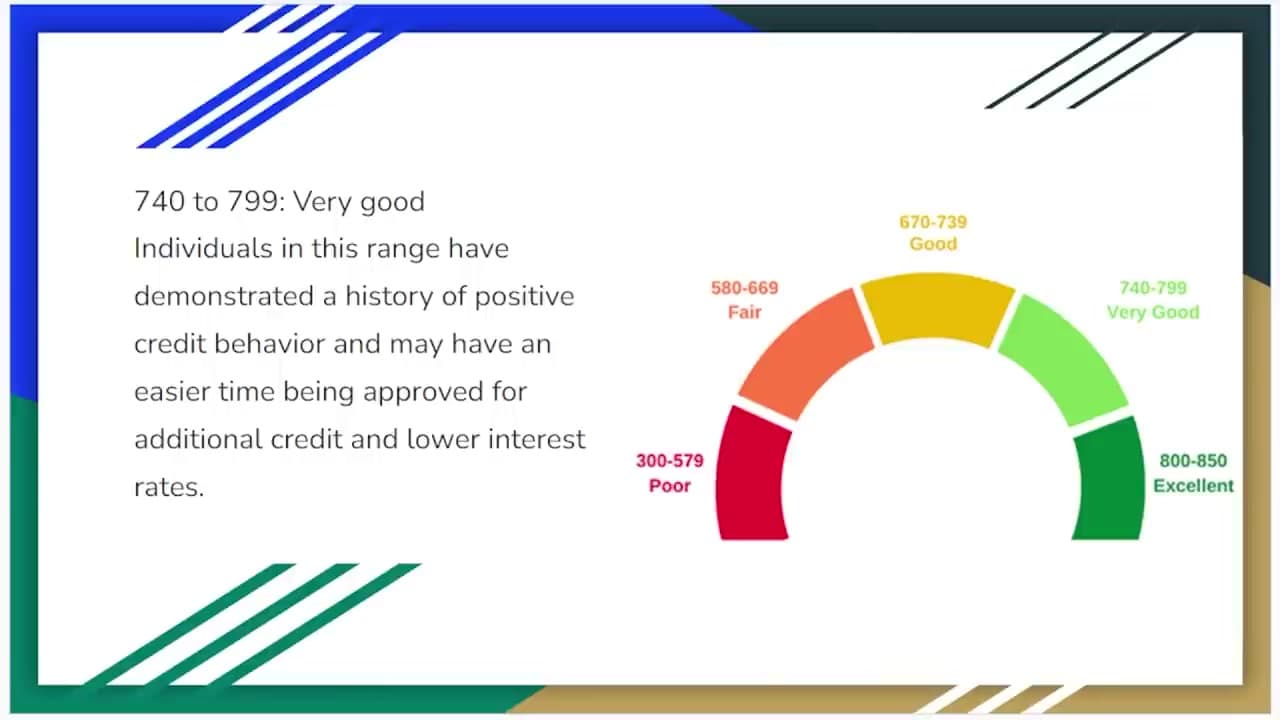

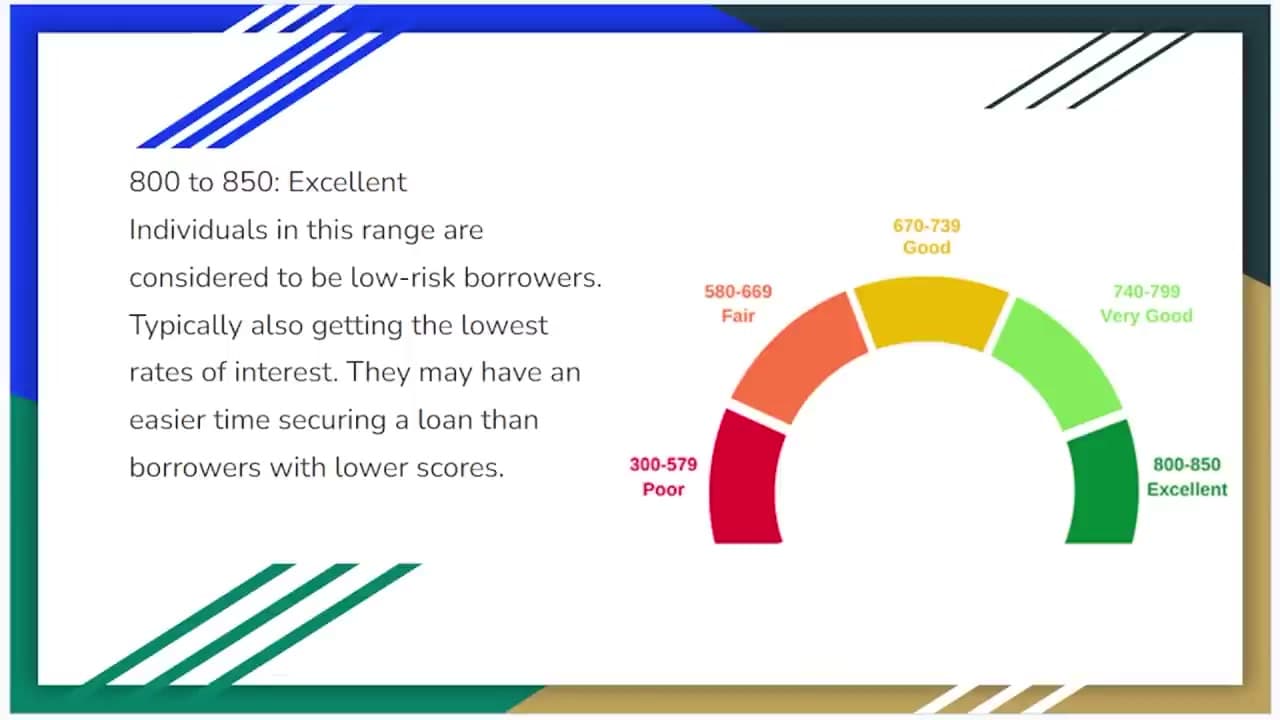

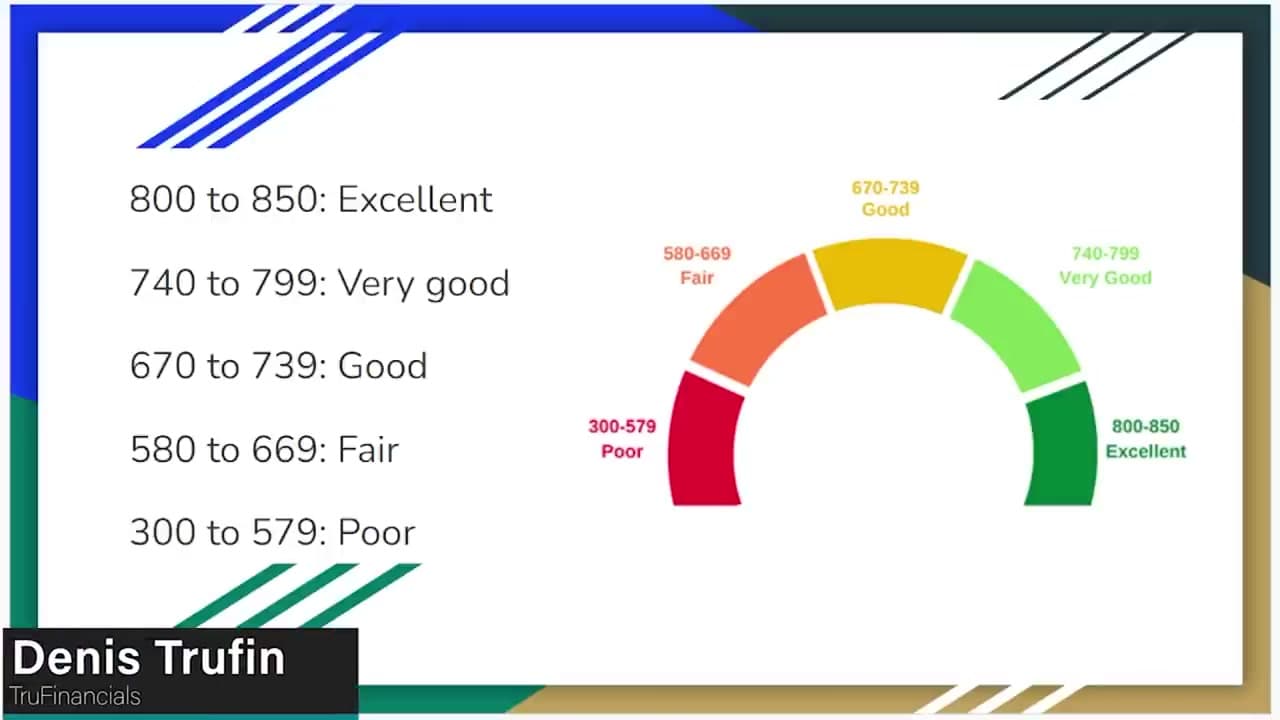

Every credit score you will ever see lives on a 300-to-850 scale. Watch the intro at 0:04. The two big scoring models, FICO and VantageScore, both use this range. FICO is the one most lenders care about - it shows up in roughly 90 percent of US lending decisions. VantageScore is what you usually see when you peek at your score through Credit Karma or your bank's free app. The two models can give you slightly different numbers from the same credit file because they weight things a little differently, but the 300 to 850 scale is the same. Three hundred is rock bottom. Eight fifty is a perfect score, and only about 1.7 percent of adults ever hit it.

Tip

Do not chase a perfect 850. Once you cross 760, almost every lender treats you the same. The difference between 760 and 850 rarely changes your interest rate.