1

Step 1: What APR Actually Is

1:52

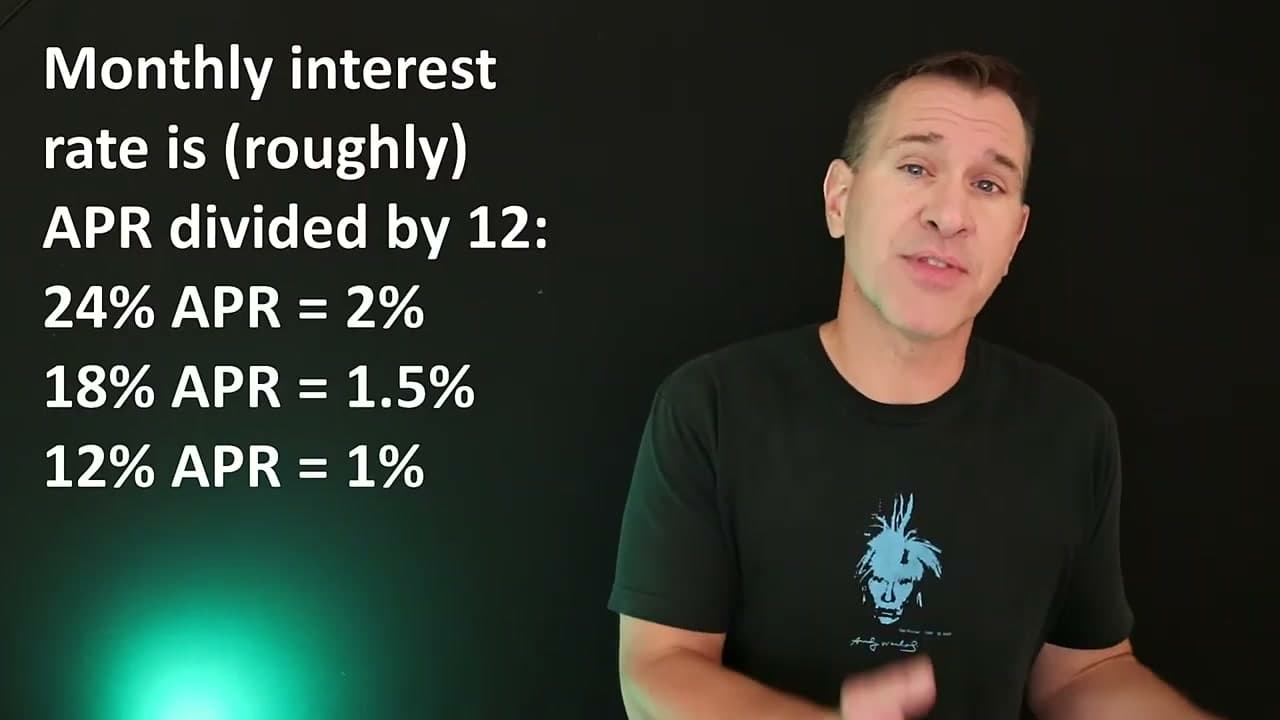

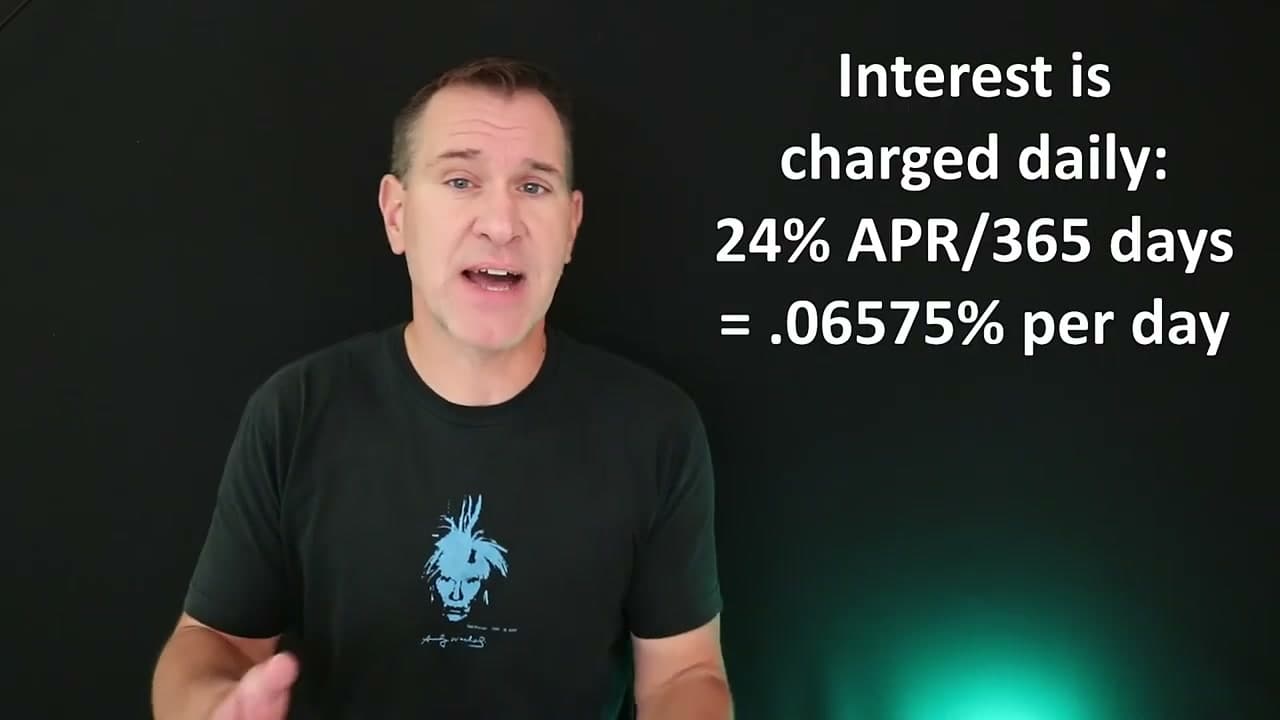

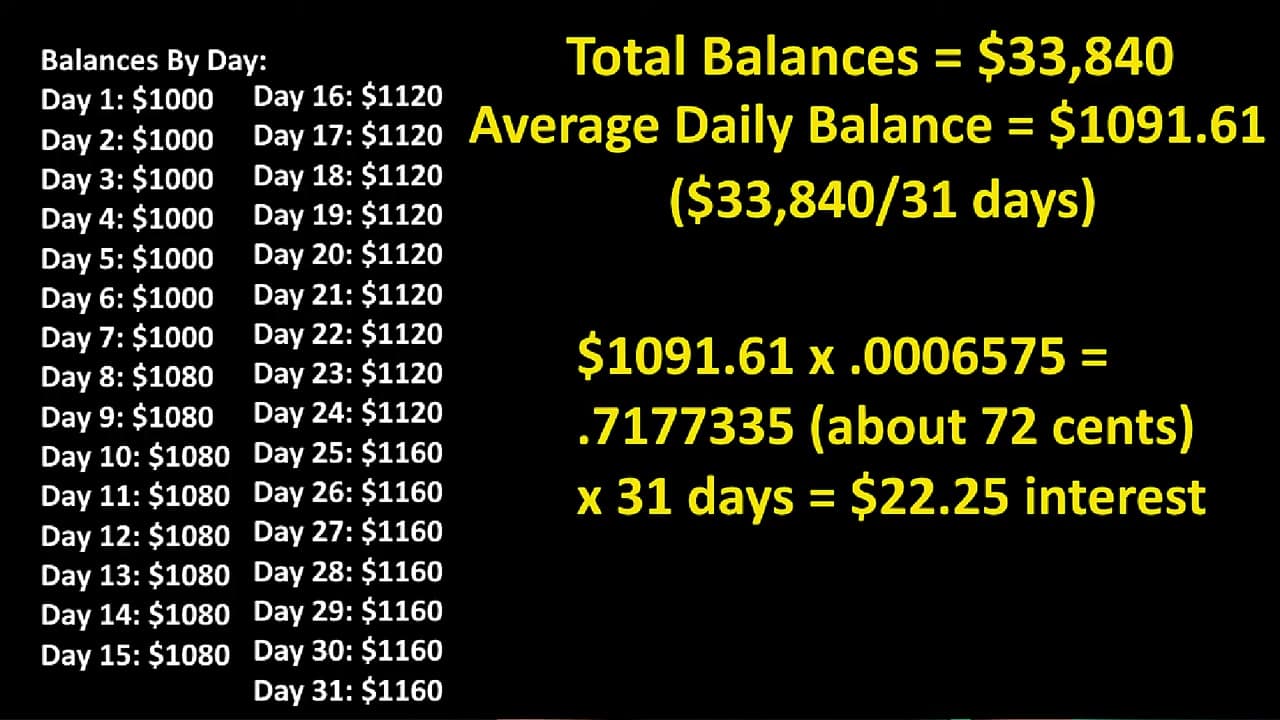

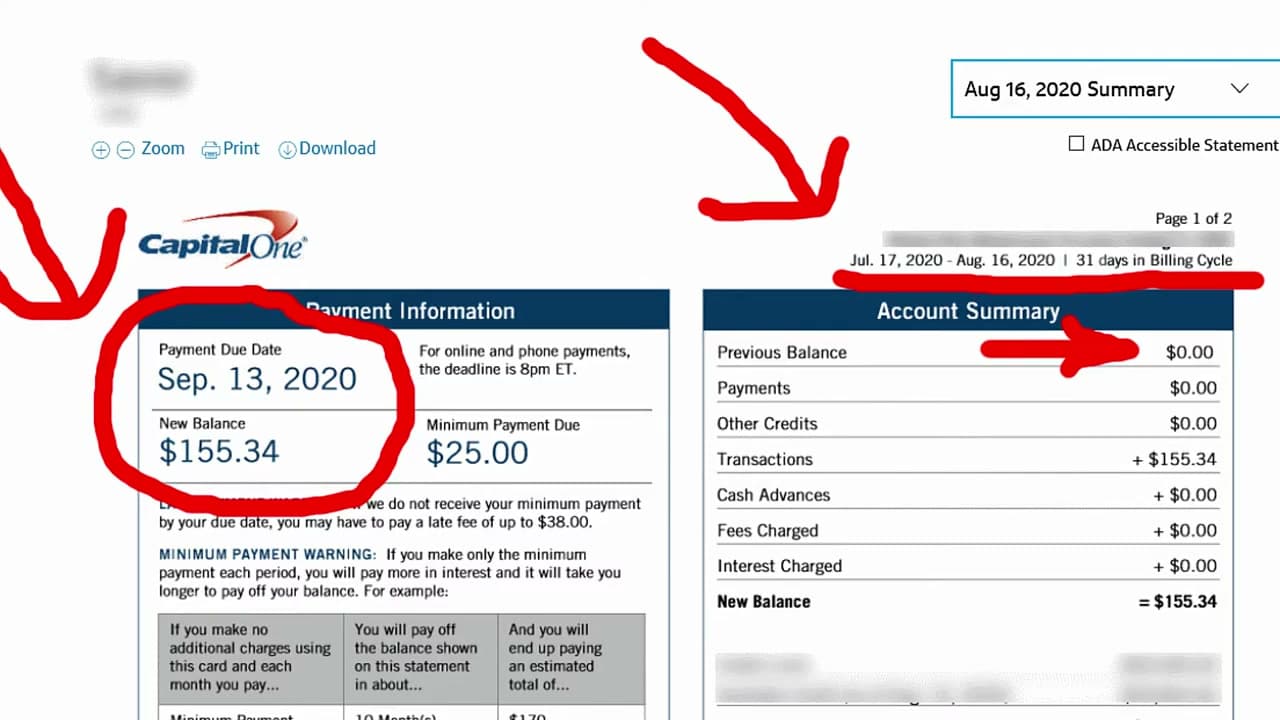

APR is the price of borrowing money on your card, written as a yearly percentage. You will find it on your statement and in your card agreement. Many cards list more than one: a purchase APR, a higher cash-advance APR, and a penalty APR if you miss payments.

The key thing to understand is that APR only matters when you carry a balance from one month to the next. On a statement where you paid everything off, the interest charged line reads zero, no matter how high the APR is.