1

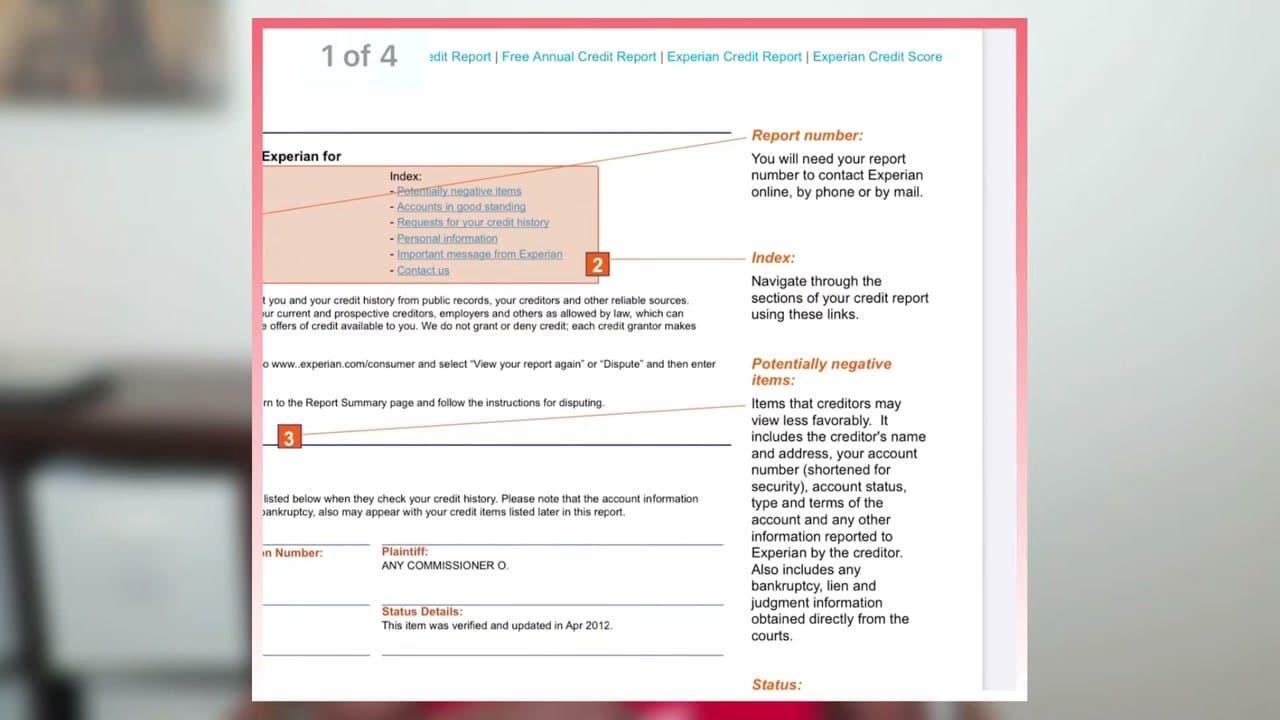

Step 1: Find Your Report Number and Index

11:40

Every credit report starts with a report number and an index of sections. Save the report number - you'll need it if you contact the bureau to dispute anything.

The index lets you jump to Potentially Negative Items, Accounts in Good Standing, Requests for Your Credit History, and Personal Information. Use it as a navigation aid - the full report can be 20+ pages on a long credit history.