1

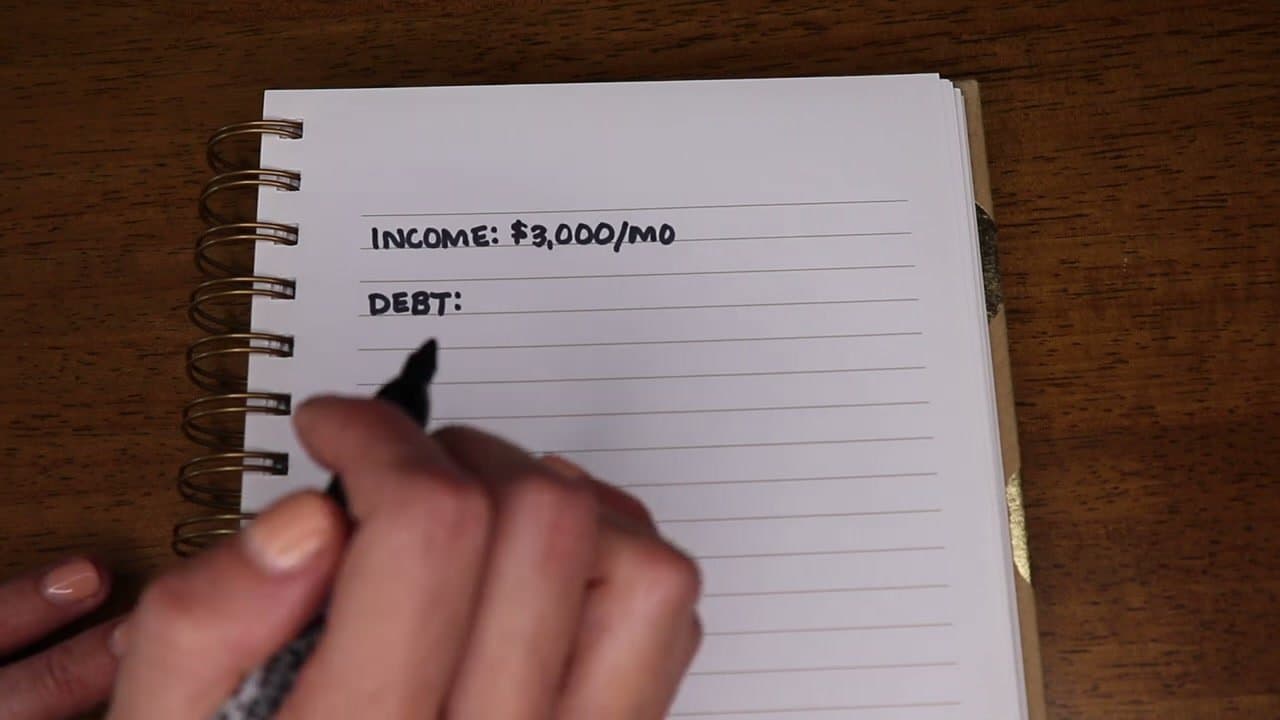

Step 1: Write Down Your Monthly Income

1:55

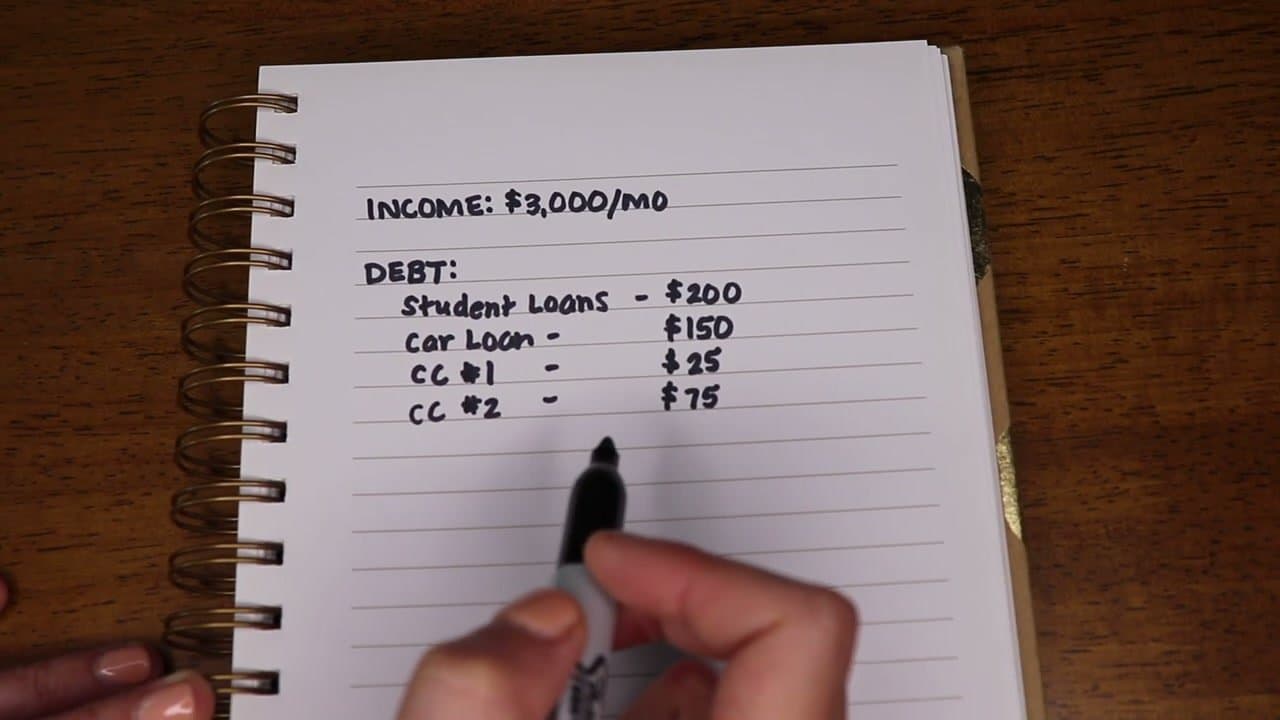

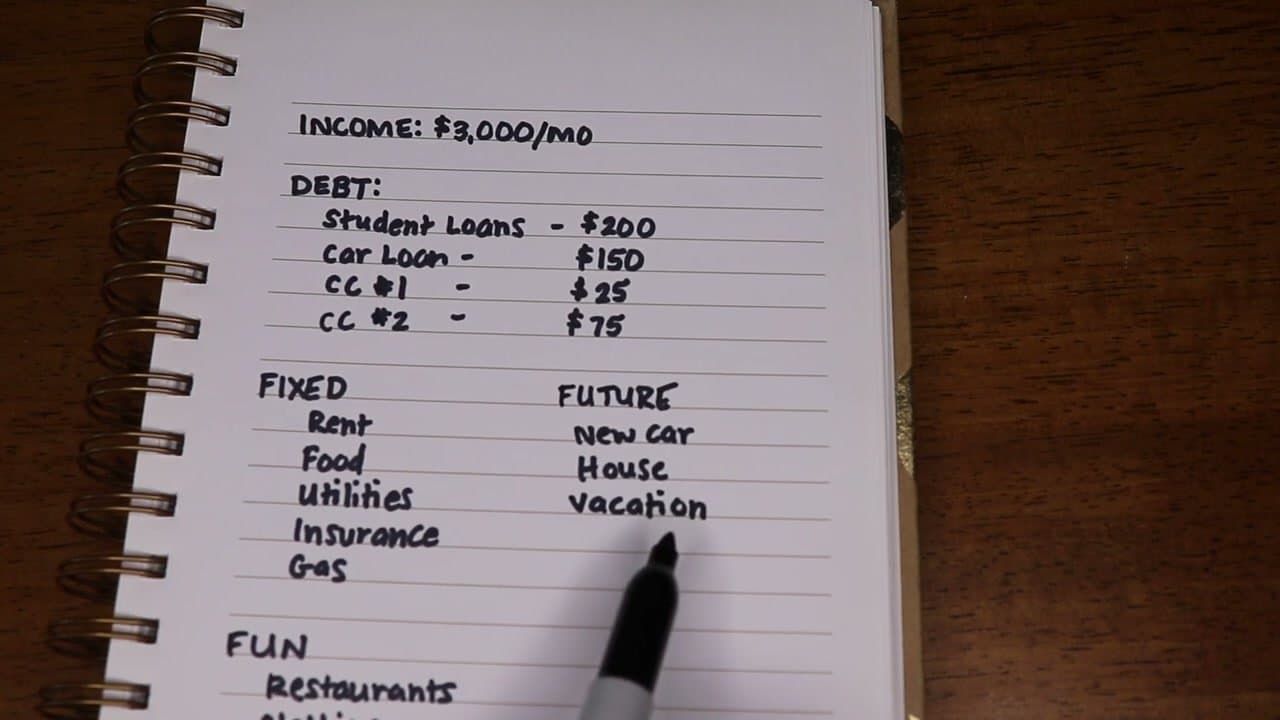

Start with a blank page and write your total monthly take-home at the top. The number you want is what actually lands in your bank account, not your gross salary - taxes and benefits are already gone.

Pull the figure straight from recent paychecks. If your hours fluctuate, average the last three months so a slow week doesn't throw the whole plan off. The example here uses a $3,000 monthly take-home.