1

Step 1: List Every Debt With Its Balance and Interest Rate

4:00

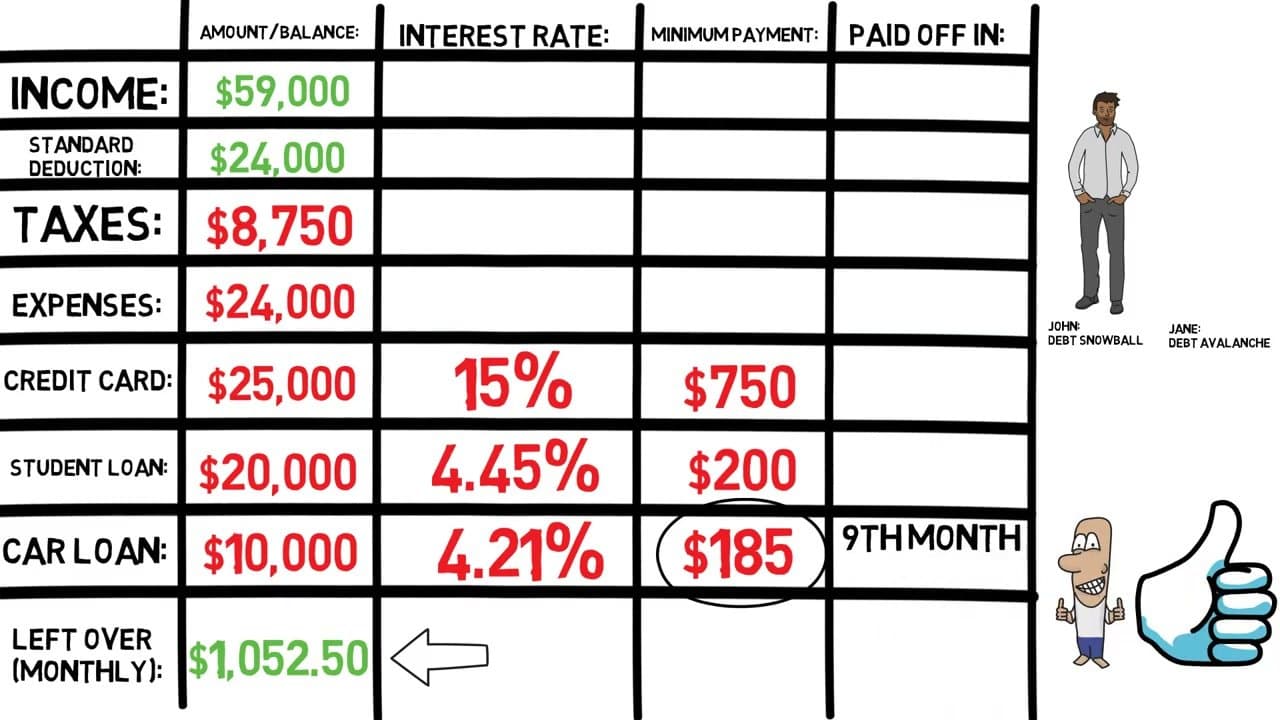

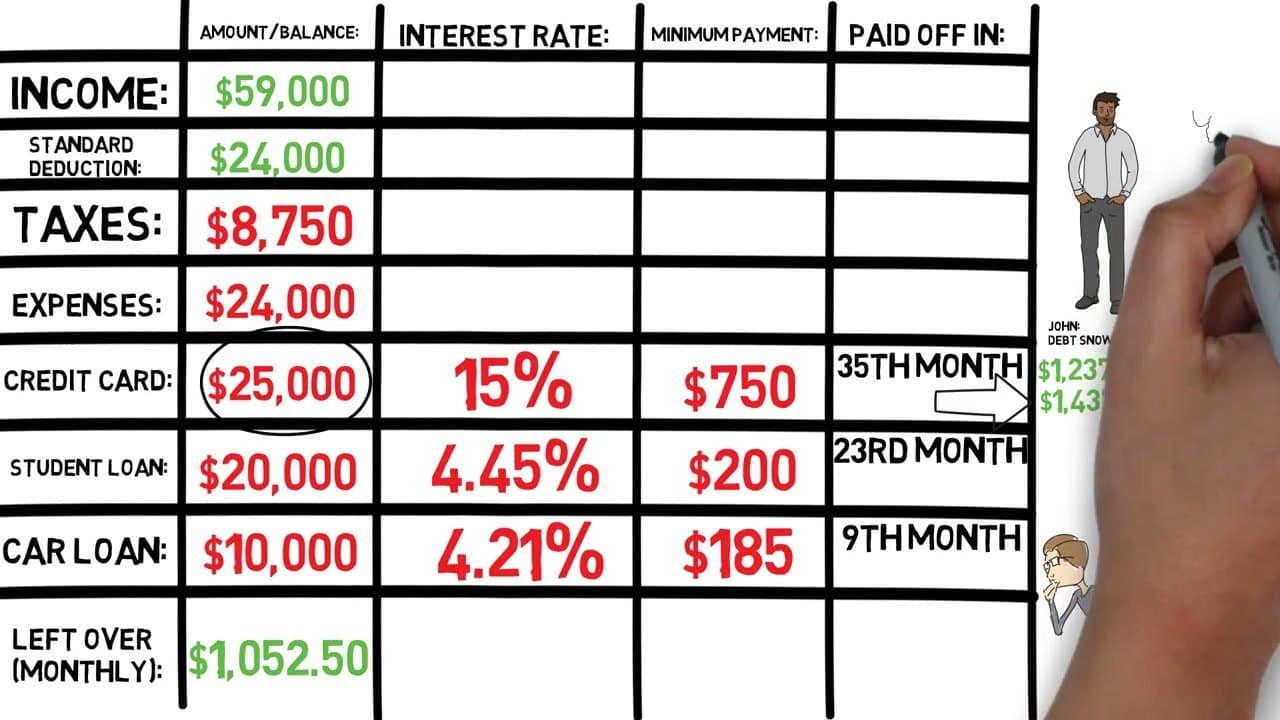

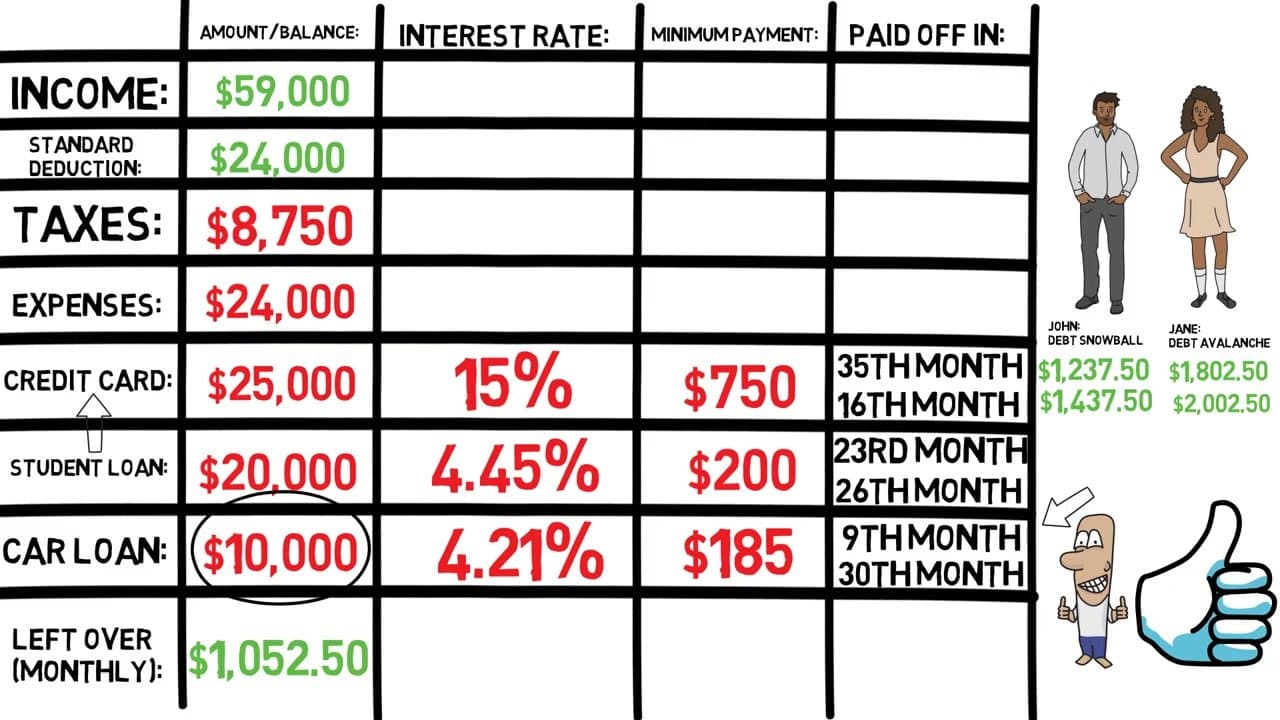

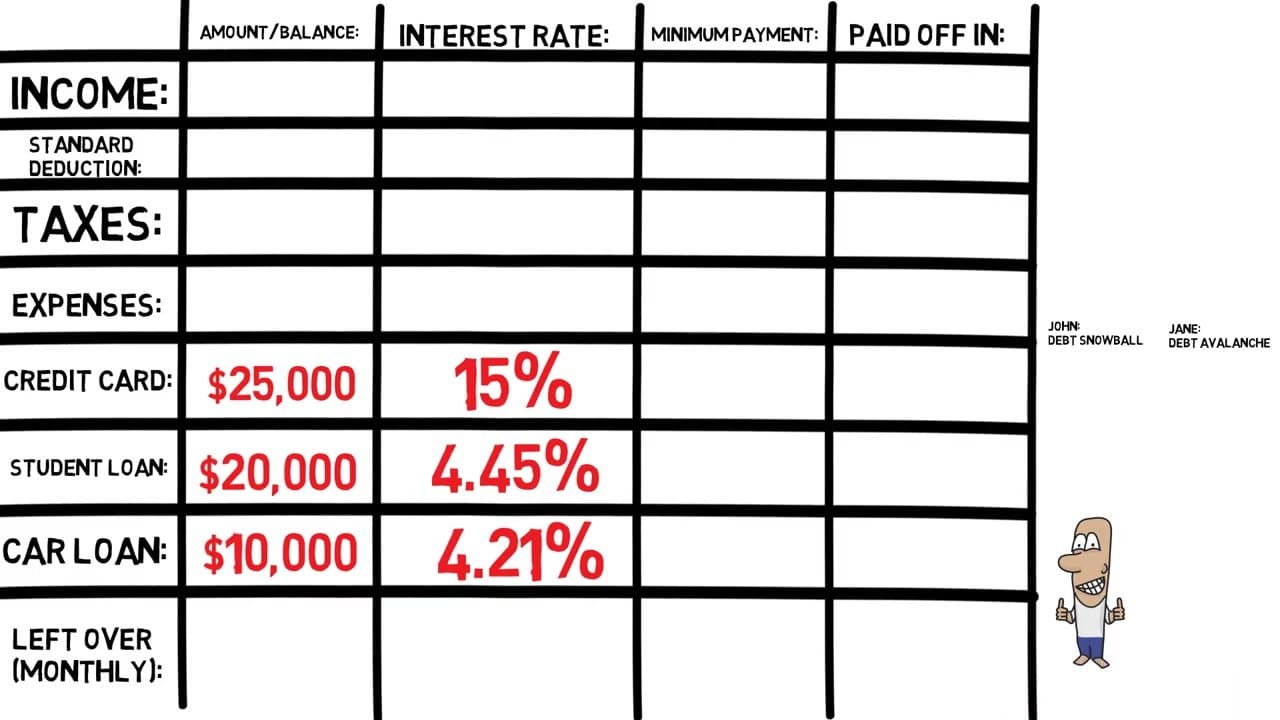

Pull a fresh statement for each debt and write four columns: name, current balance, interest rate, and minimum payment. The example here uses three debts: a $25,000 credit card at 15%, a $20,000 student loan at 4.45%, and a $10,000 car loan at 4.21%.

You can't pick a strategy until everything is on one page. Most people are surprised by how the totals stack up - which is exactly the discomfort that drives the payoff plan.