Step 1: Run Your Finances Like a Business

0:36

Before you write a single number down, just look at your accounts. A study out of Rice University found that simple self-awareness about your money - knowing what you have, what you owe, what you spend - is the single biggest driver of financial progress. Not income, not budgeting apps, not willpower. Awareness.

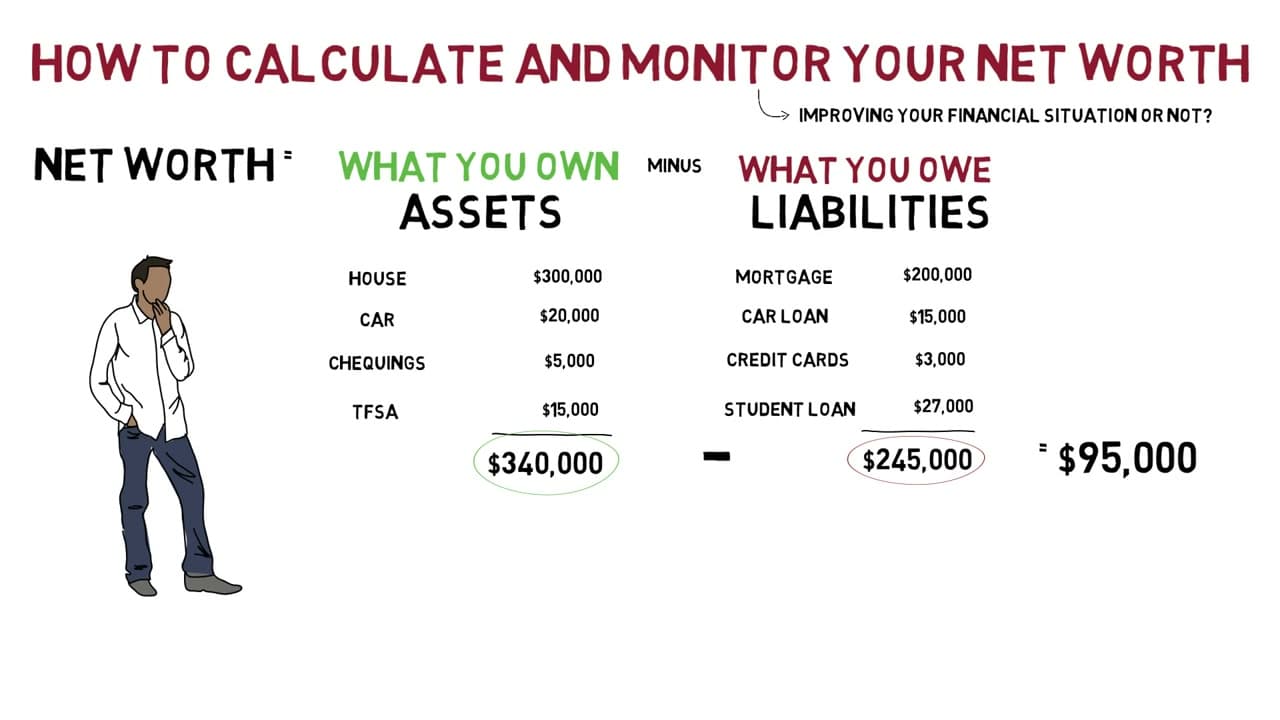

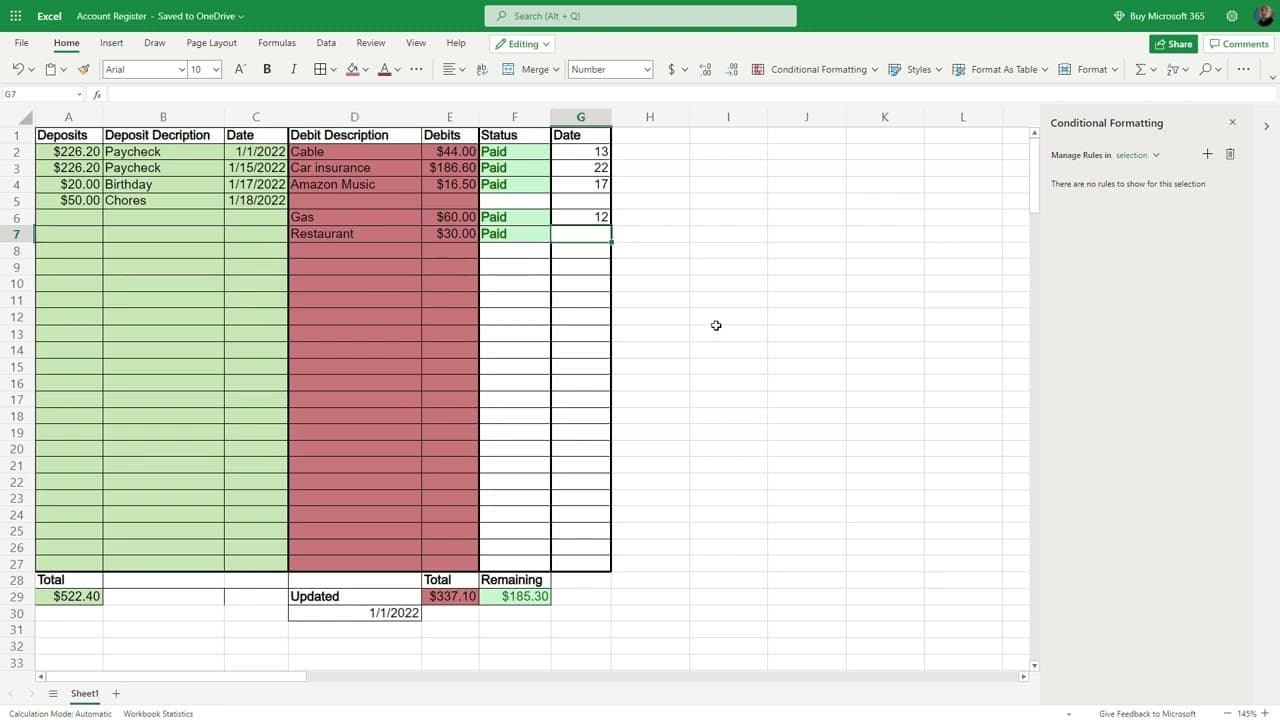

Pull up every account you own: checking, savings, credit cards, student loans, car loan, retirement, brokerage. Write the current balance for each on one page. No plan yet. No judgment. You're taking inventory so the budget you build next is grounded in real numbers instead of a hopeful guess.

Tip

Check balances at least once a week, even after the budget is running. Humphrey checks his every day or two - he says the peace of mind is worth more than the few minutes it costs.