1

Step 1: What Net Worth Actually Means

0:20

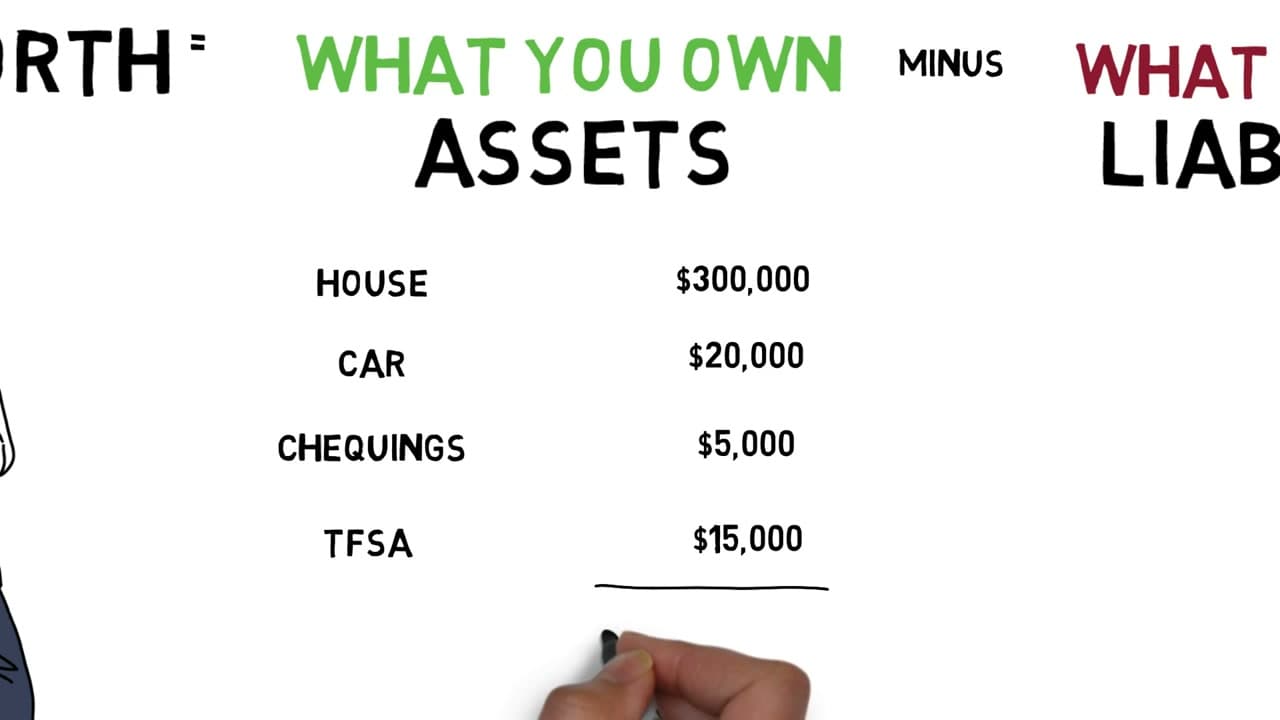

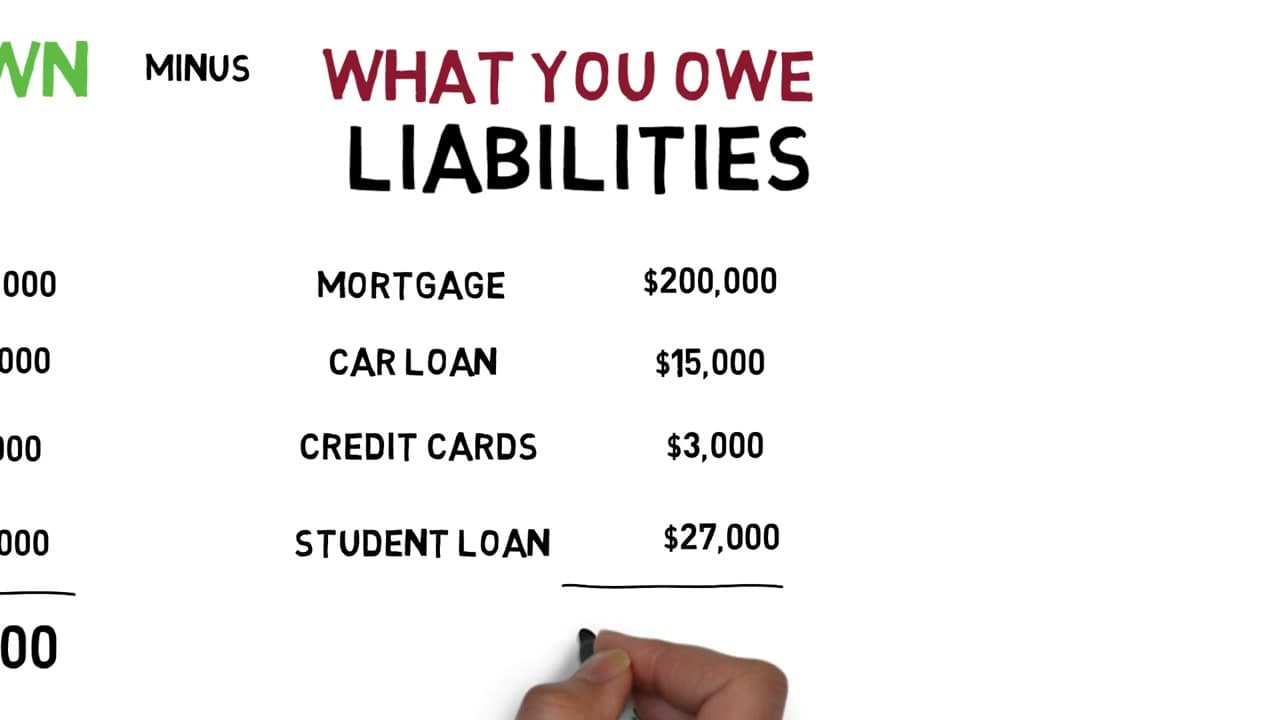

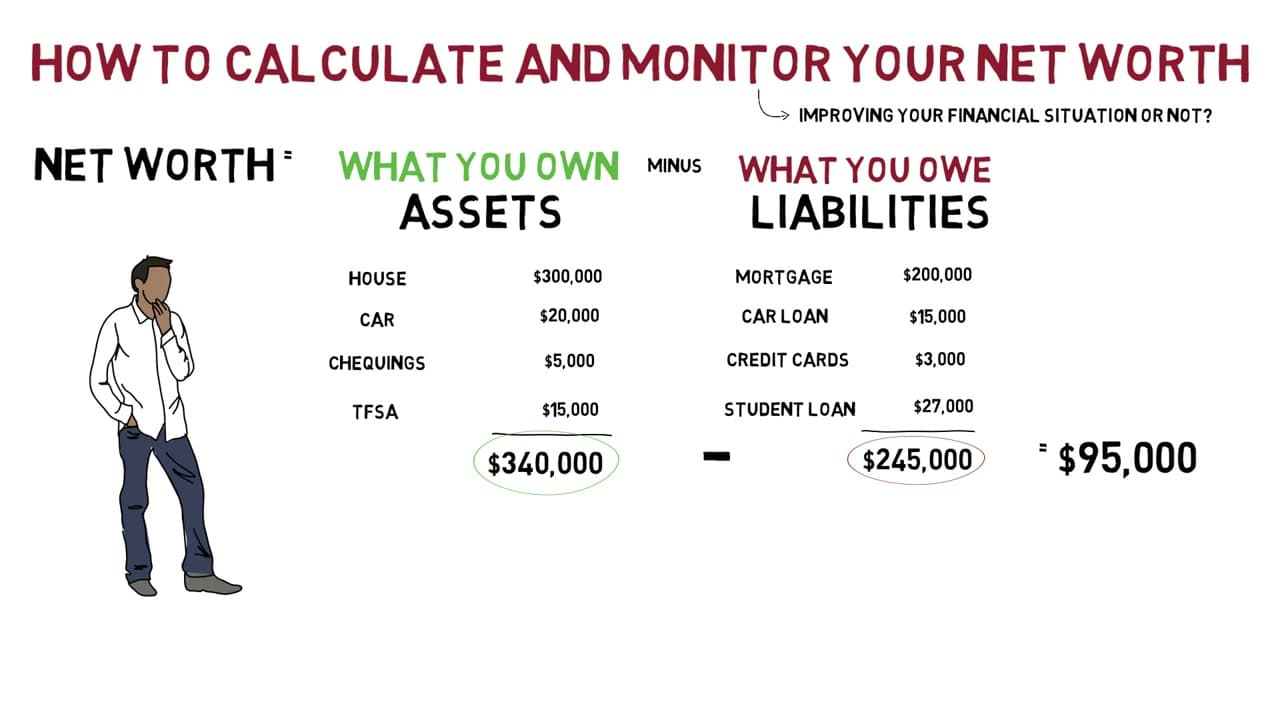

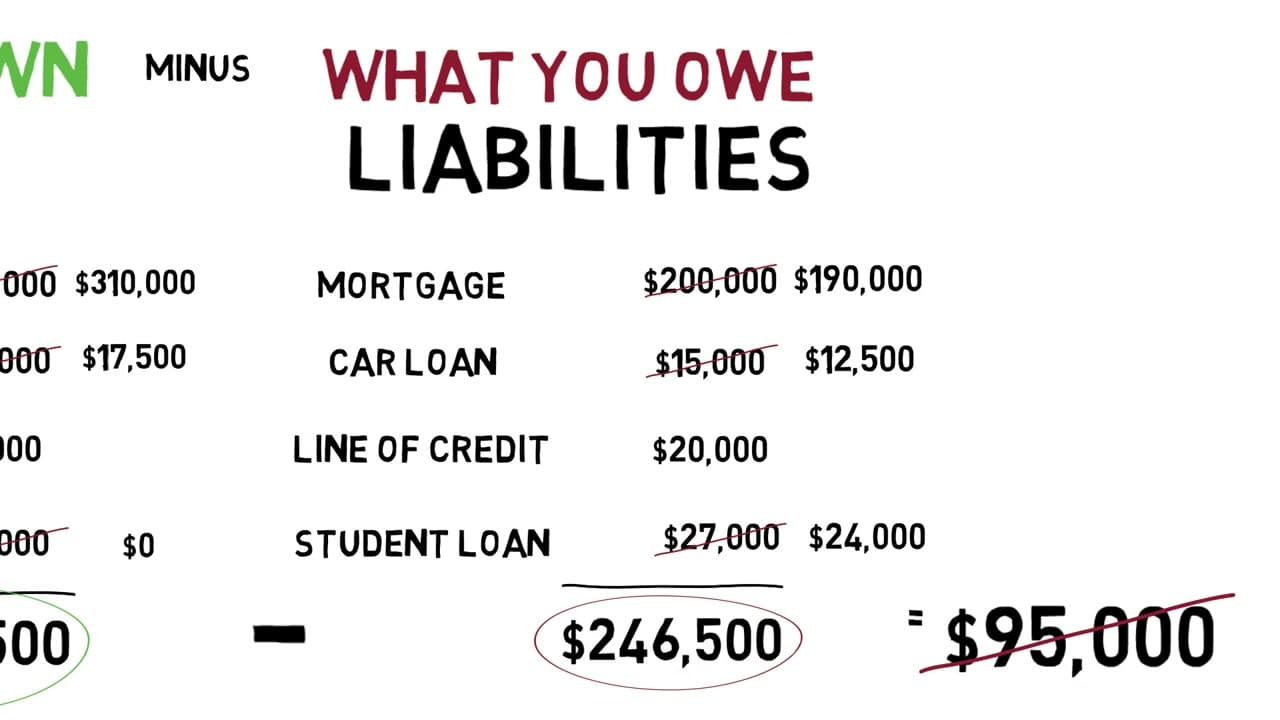

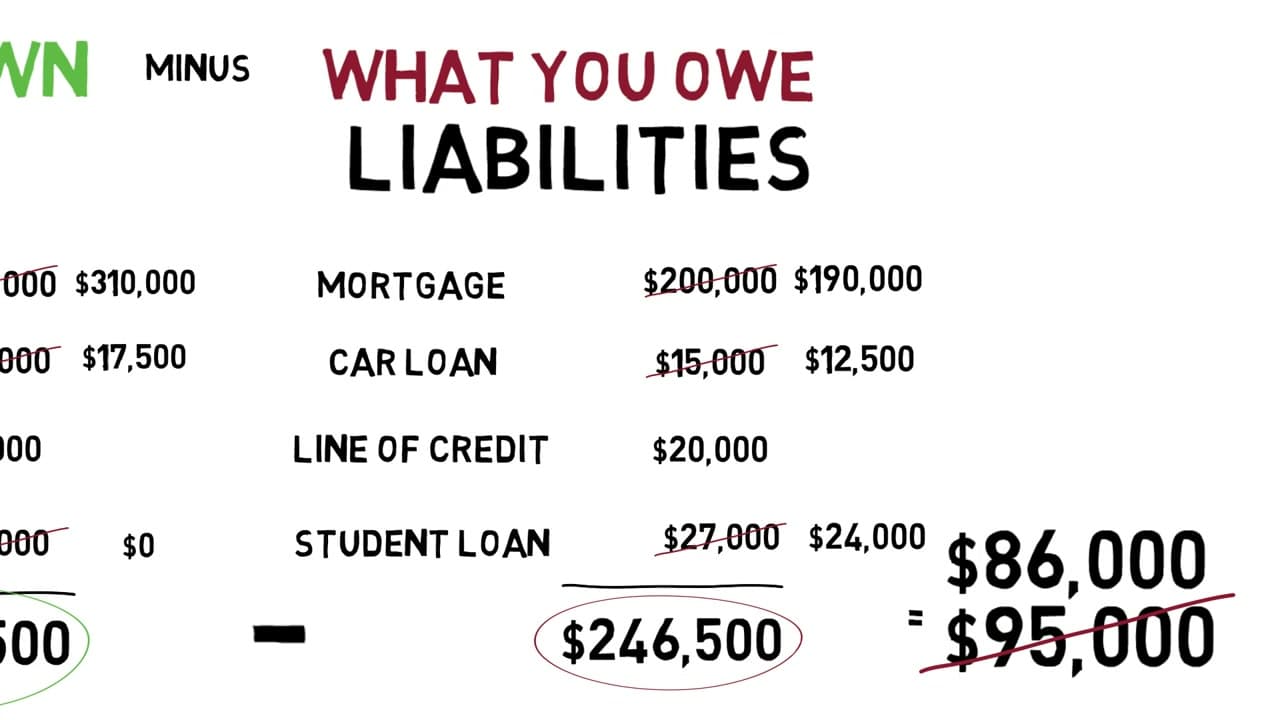

Net worth is a snapshot of your financial position on a given day. The formula never changes: what you own minus what you owe. The things you own are called your assets. The money you owe is called your liabilities.

That is it. A big paycheck does not decide your net worth, and neither does an expensive car. What matters is the gap between the value of what you hold and the debts hanging over it. Get comfortable with those two words, assets and liabilities, and the rest is arithmetic.