1

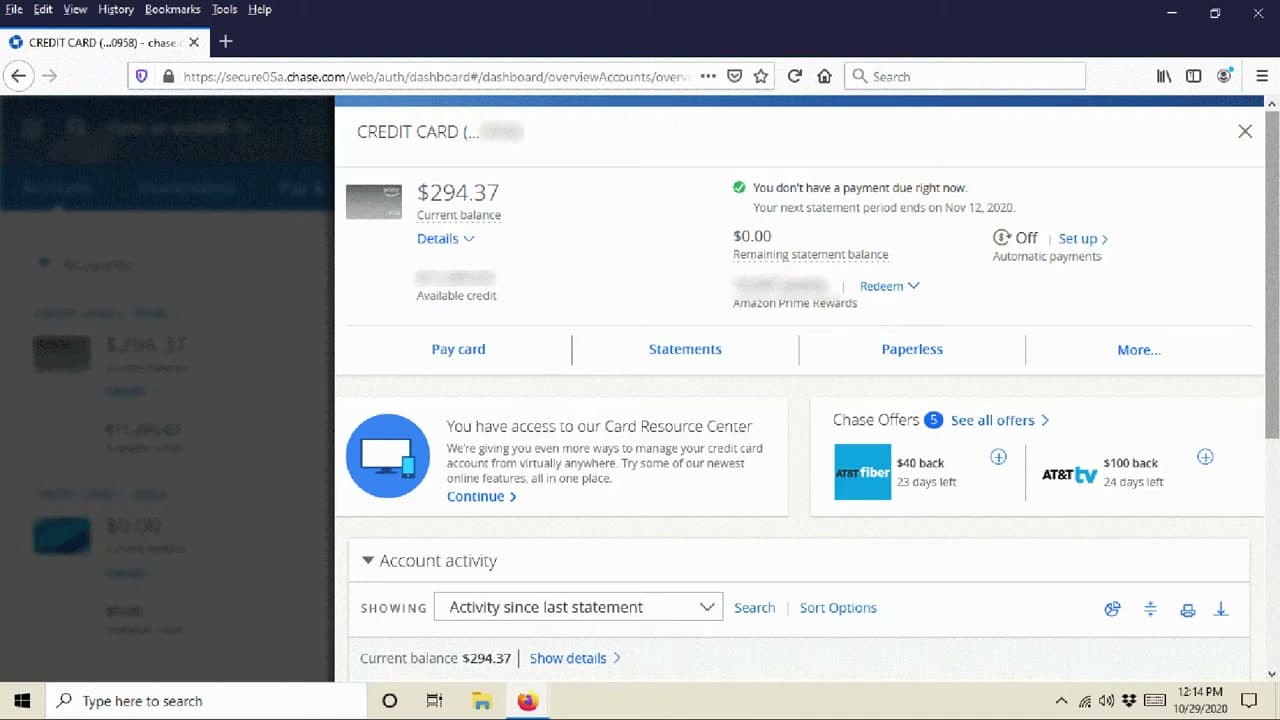

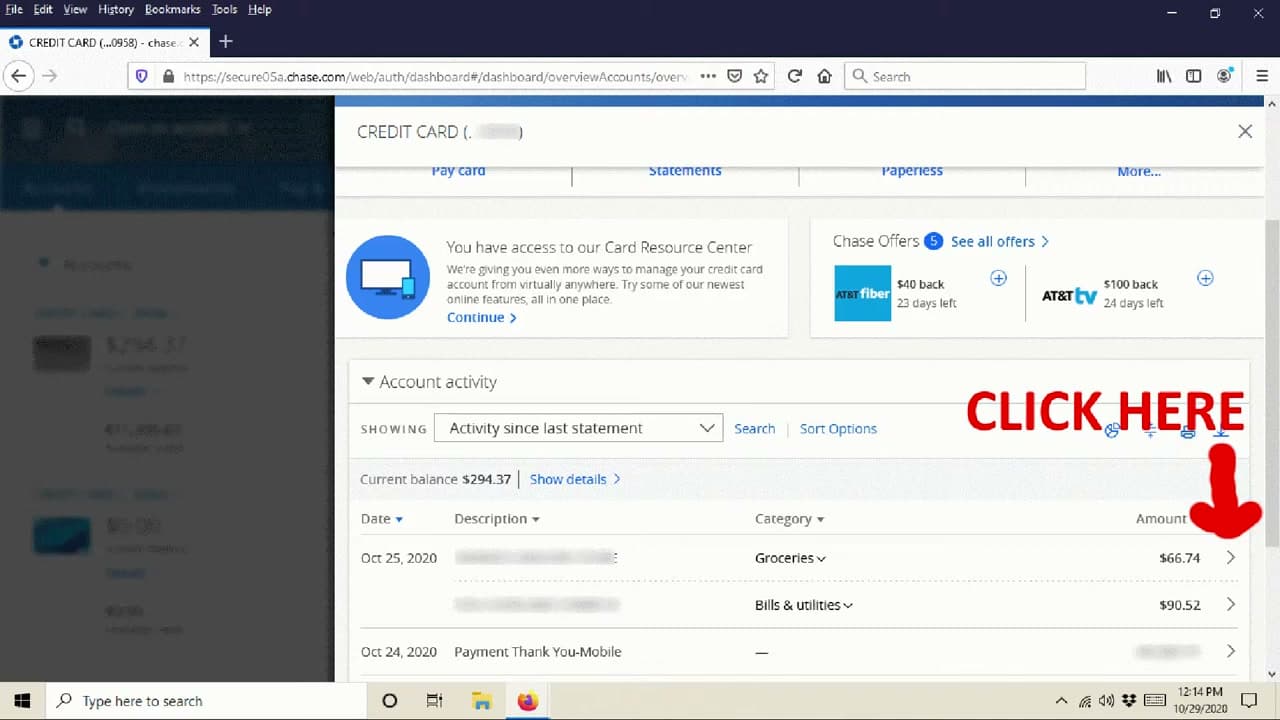

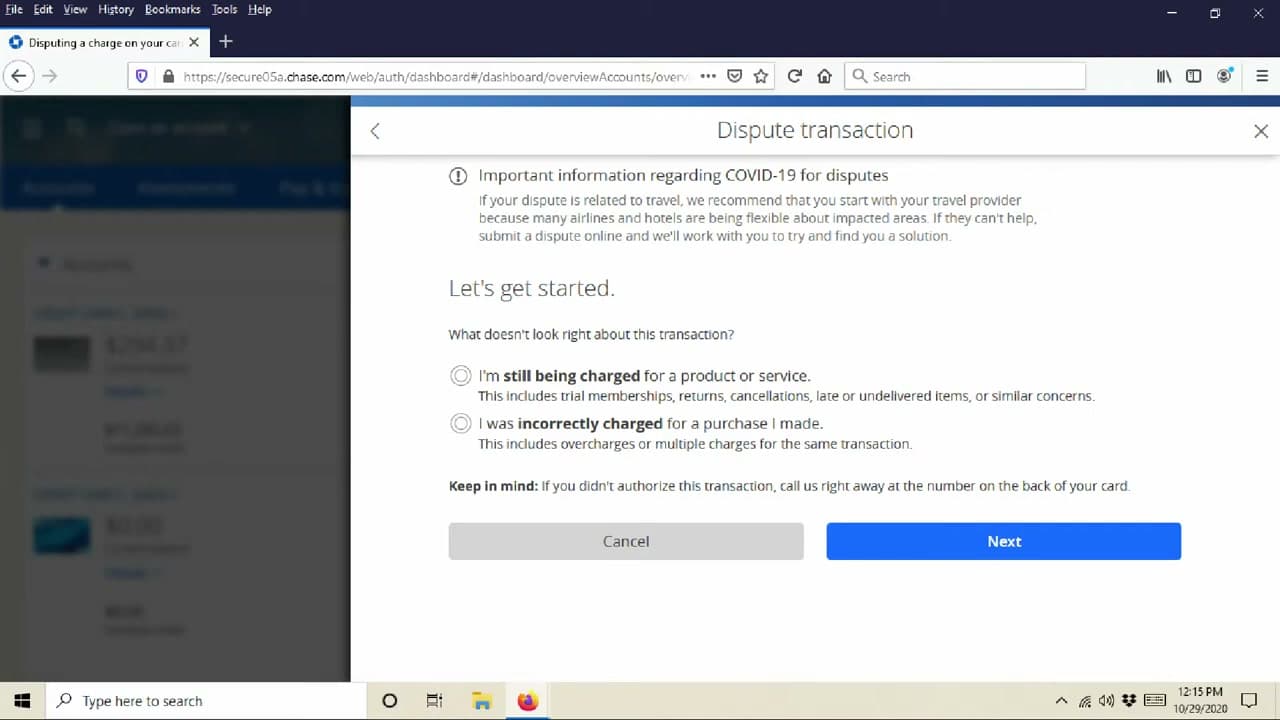

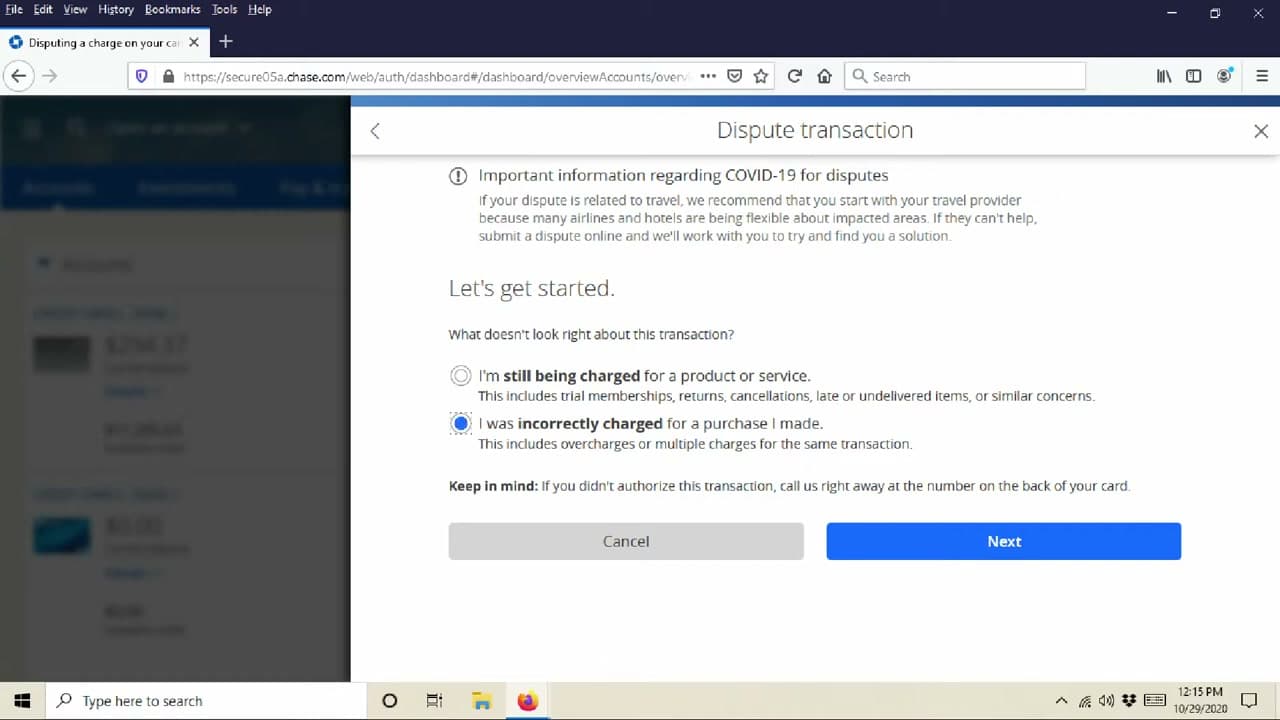

Step 1: Log Into Your Bank Account and Find the Card

0:26

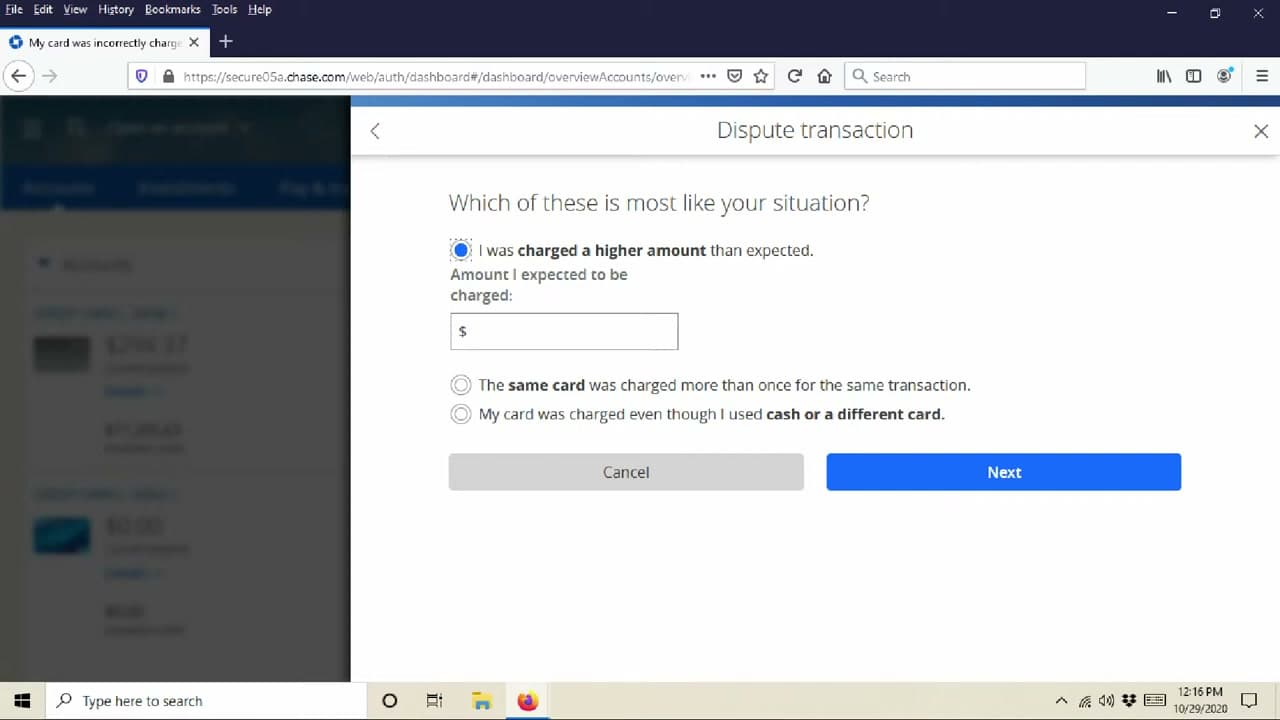

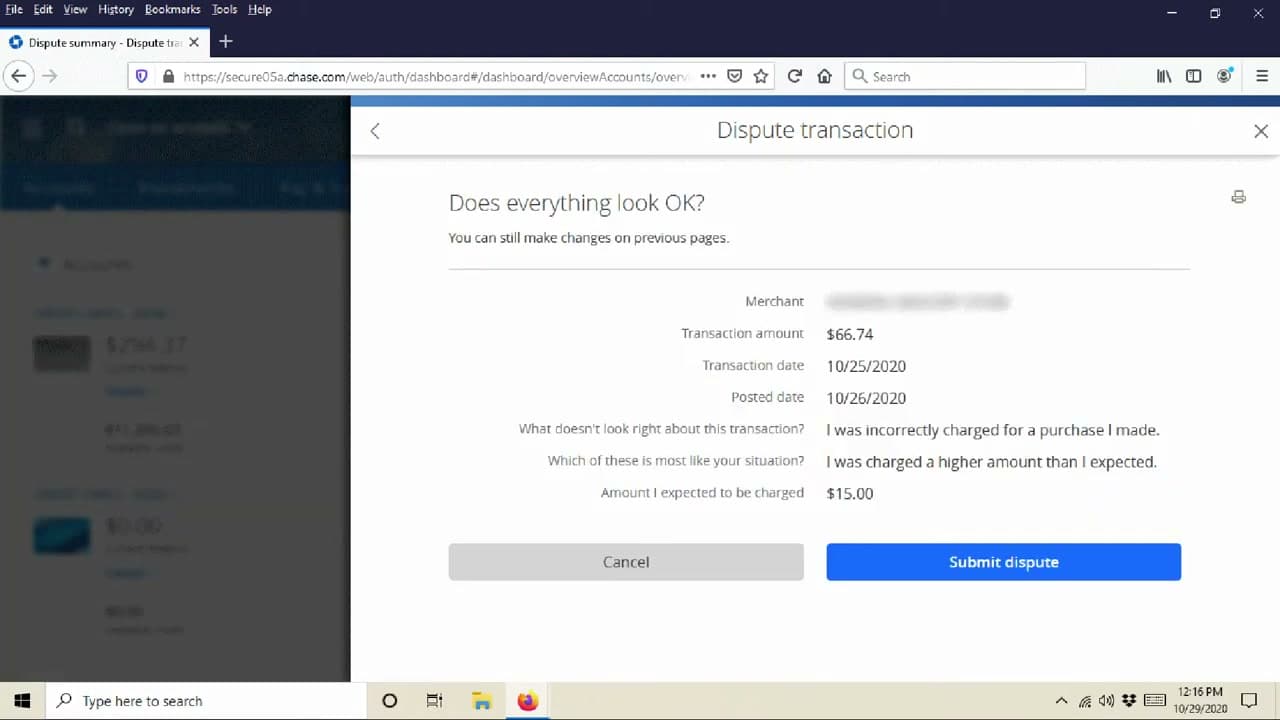

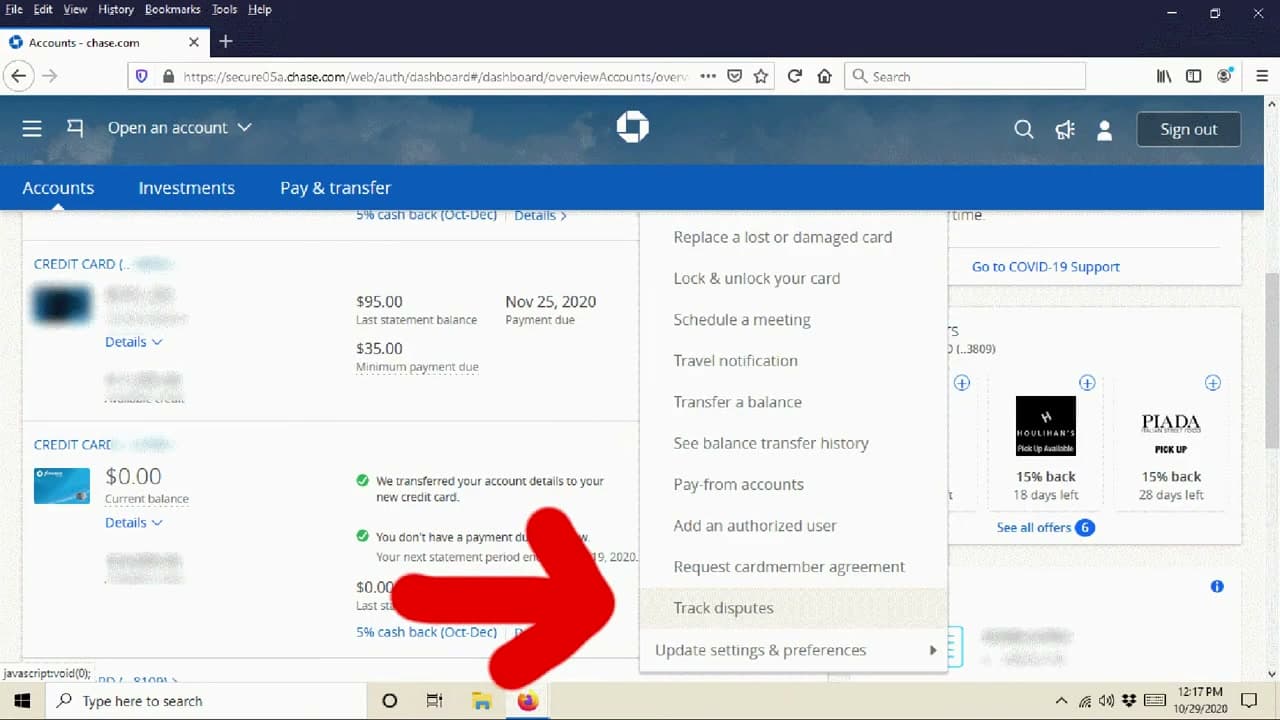

Sign into your bank or card issuer's website or mobile app with your usual login. Once you're in, you'll see a list of your cards and accounts. If you have more than one card, find the specific card the disputed charge was made on. Click or tap that card to open the account details. The walkthrough here shows Chase, but the layout is similar across most major card issuers like Capital One, Citi, and Bank of America.

Tip

Always log in through the official app or by typing the bank URL directly. Phishing emails that look like dispute notices are a common scam right around the time real disputes are happening.