1

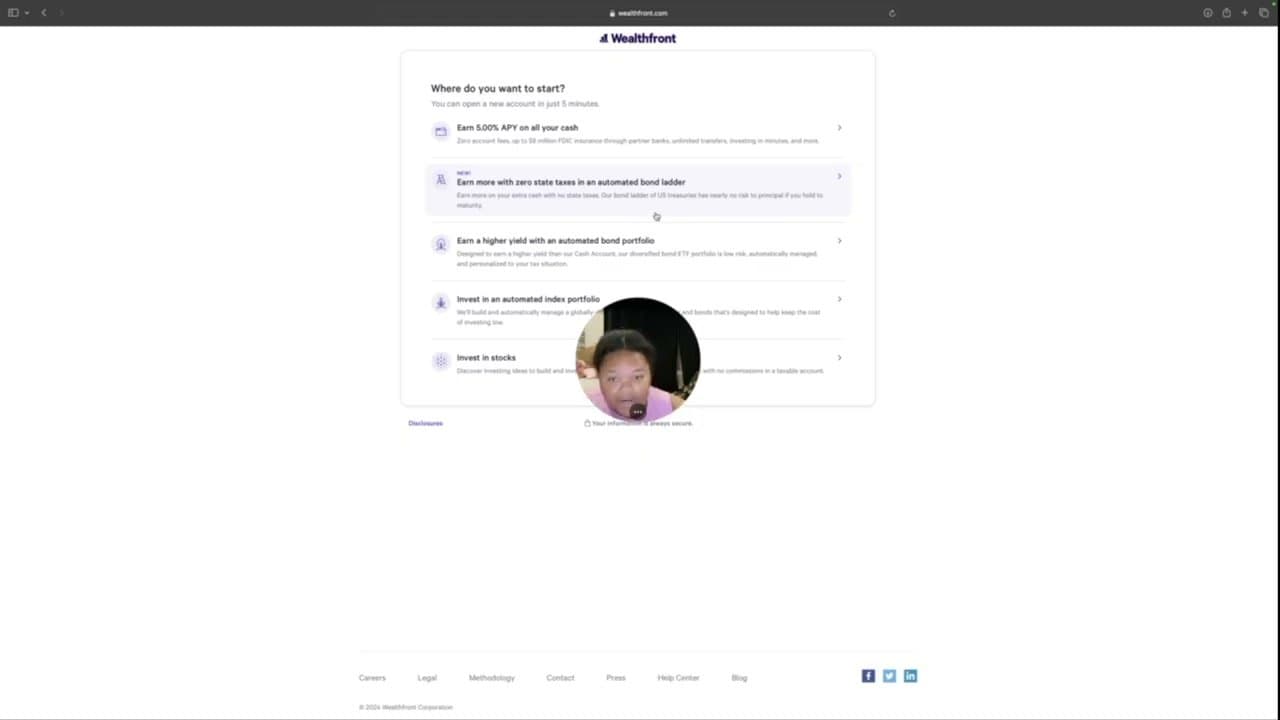

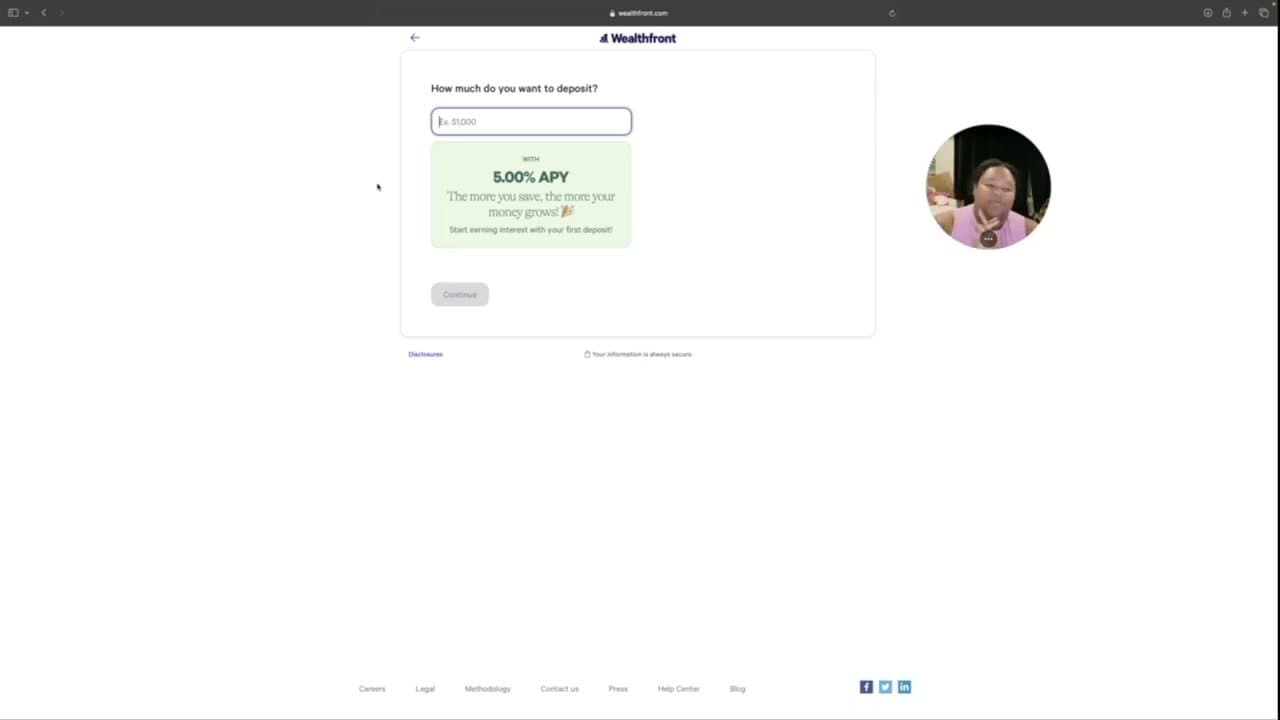

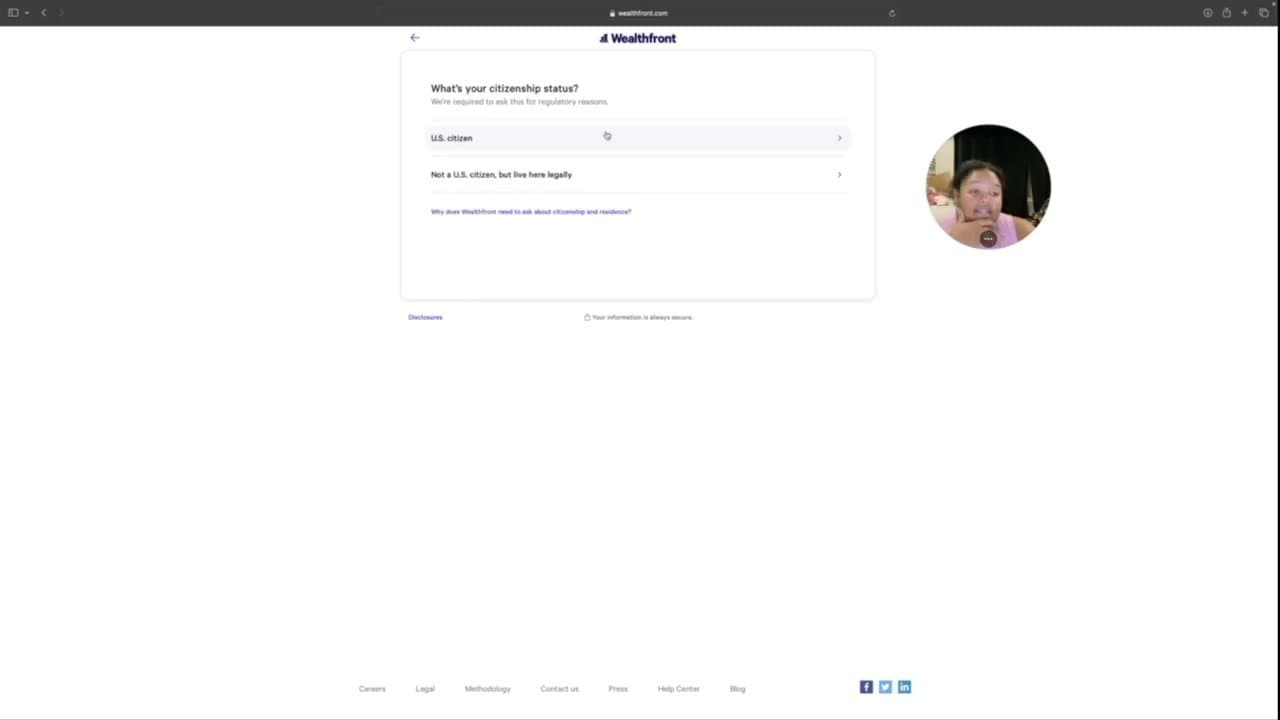

Step 1: Pick a High-Yield Account and Click Get Started

0:30

Go to your chosen high-yield savings provider. The trick is to pick one with no monthly fees, no minimum balance, and an APY at least 10x what your big bank offers. Wealthfront in this walkthrough pays 5.00% APY with no fees and FDIC insurance up to $8 million through partner banks.

Click Get Started in the top right.