1

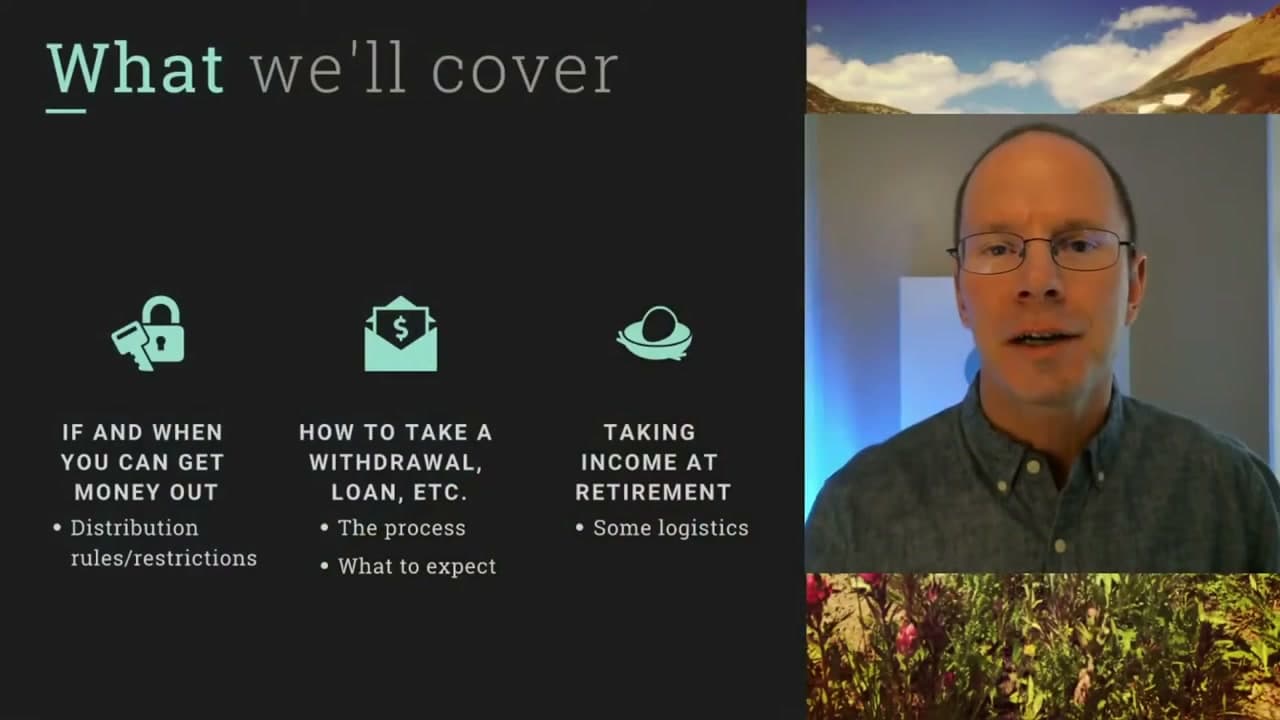

Step 1: Check Whether Your 401(k) Plan Even Allows a Withdrawal

0:14

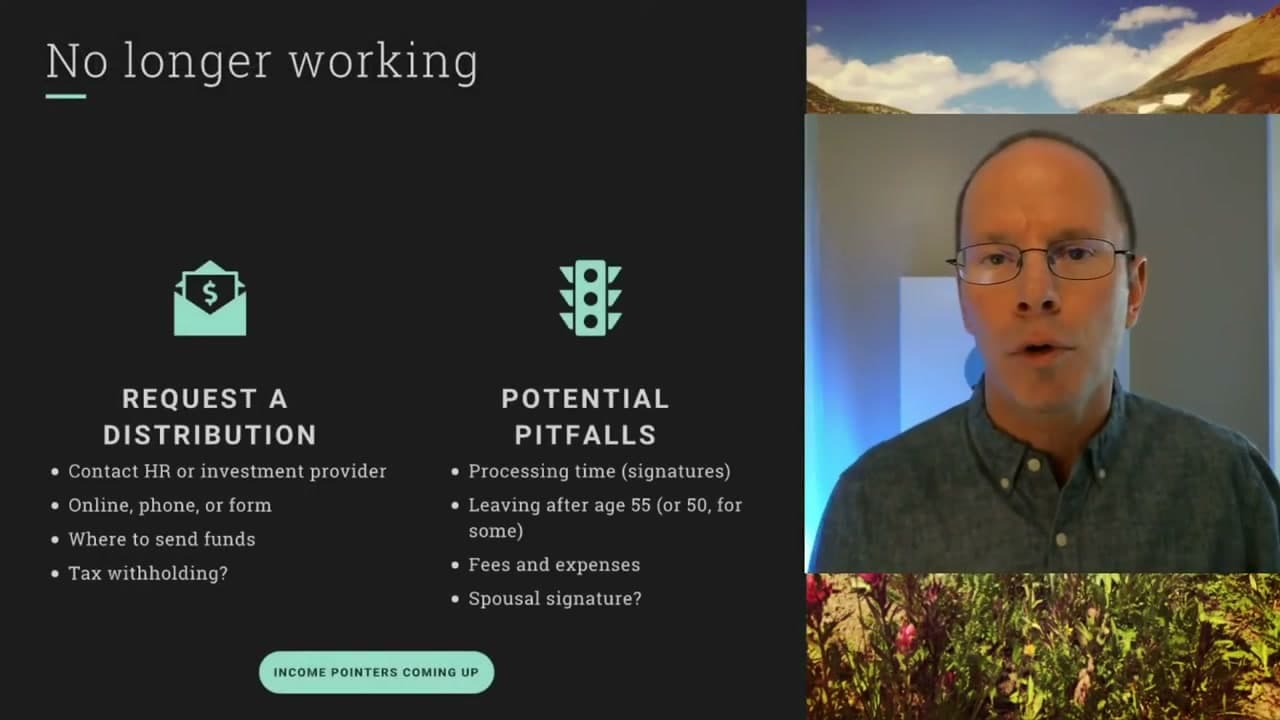

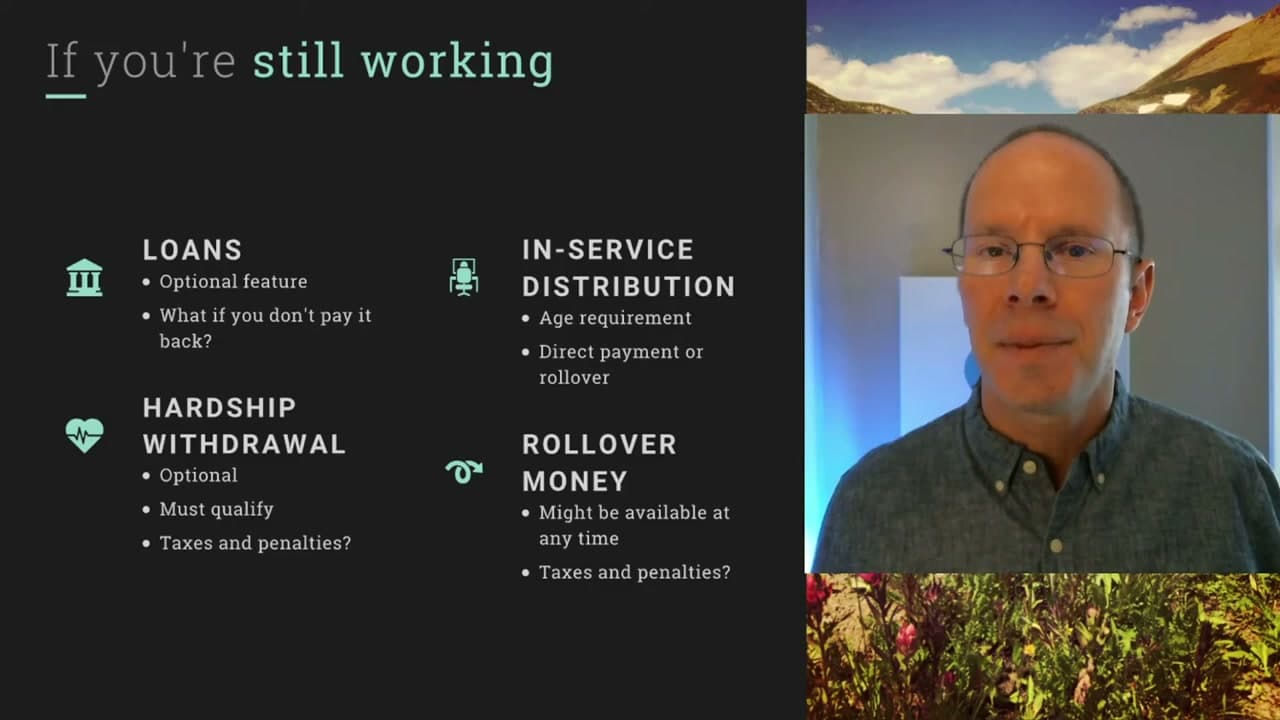

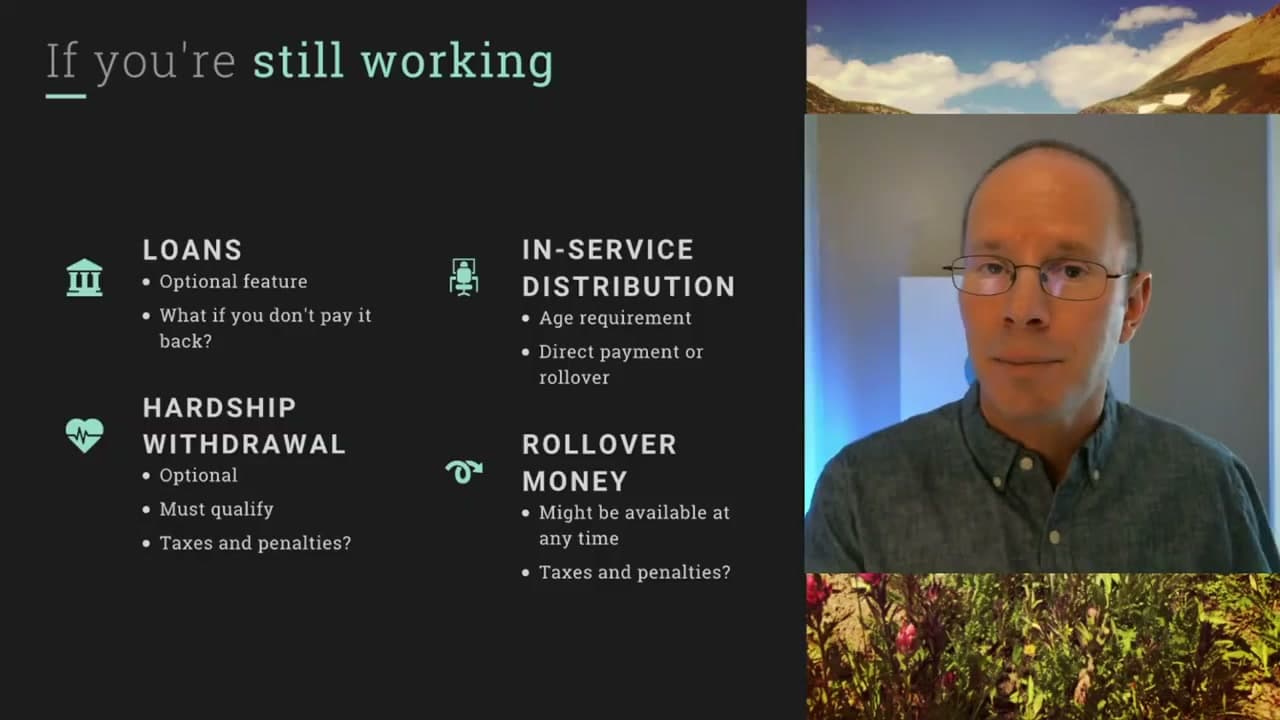

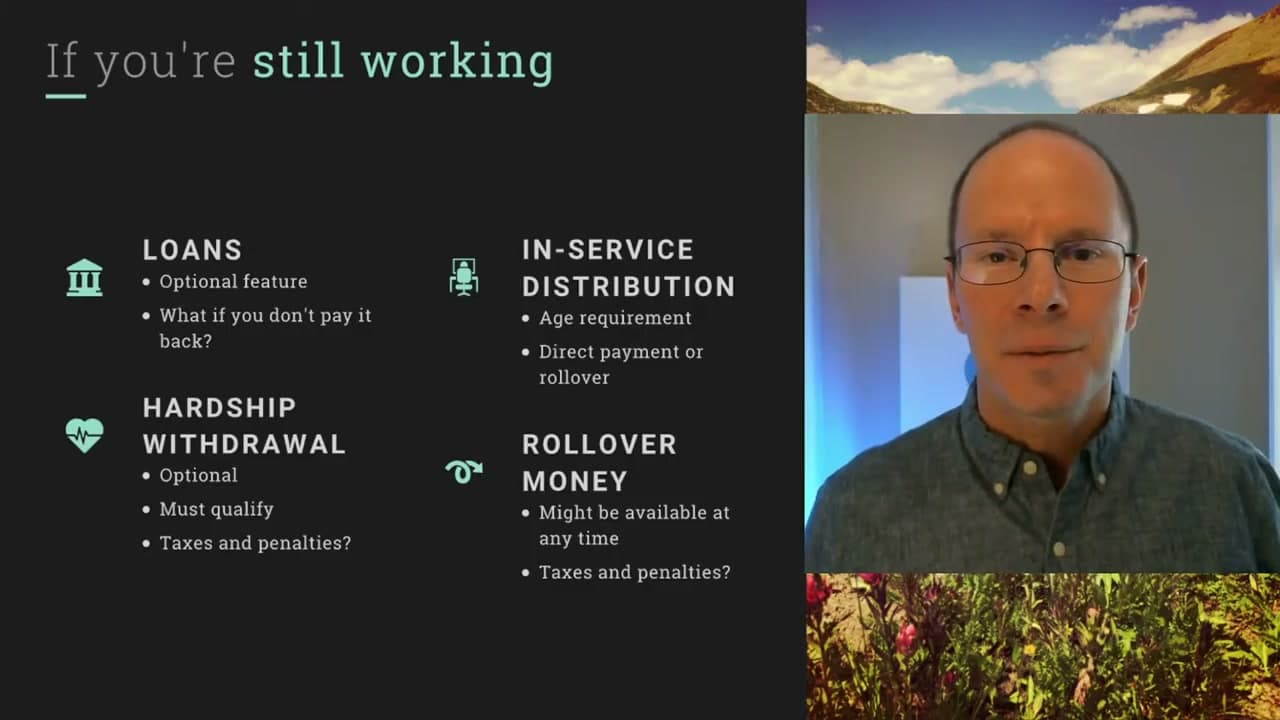

Start here, because the rules depend on your situation. 401(k) plans set limits on when you can pull money out, and the answer splits into two cases: you are still working at the employer that sponsors the plan, or you have already left that job.

If you have left, withdrawals are usually straightforward. If you are still working, your access is limited to whatever optional features your employer chose to include in the plan. Pull up your Summary Plan Description or call your benefits department and ask what is actually available to you.

Tip

Don't assume every 401(k) plan offers loans, hardship distributions, or in-service withdrawals. Plans differ a lot.