Step 1: Why You Cannot Just Trust the SSA Estimate

0:52

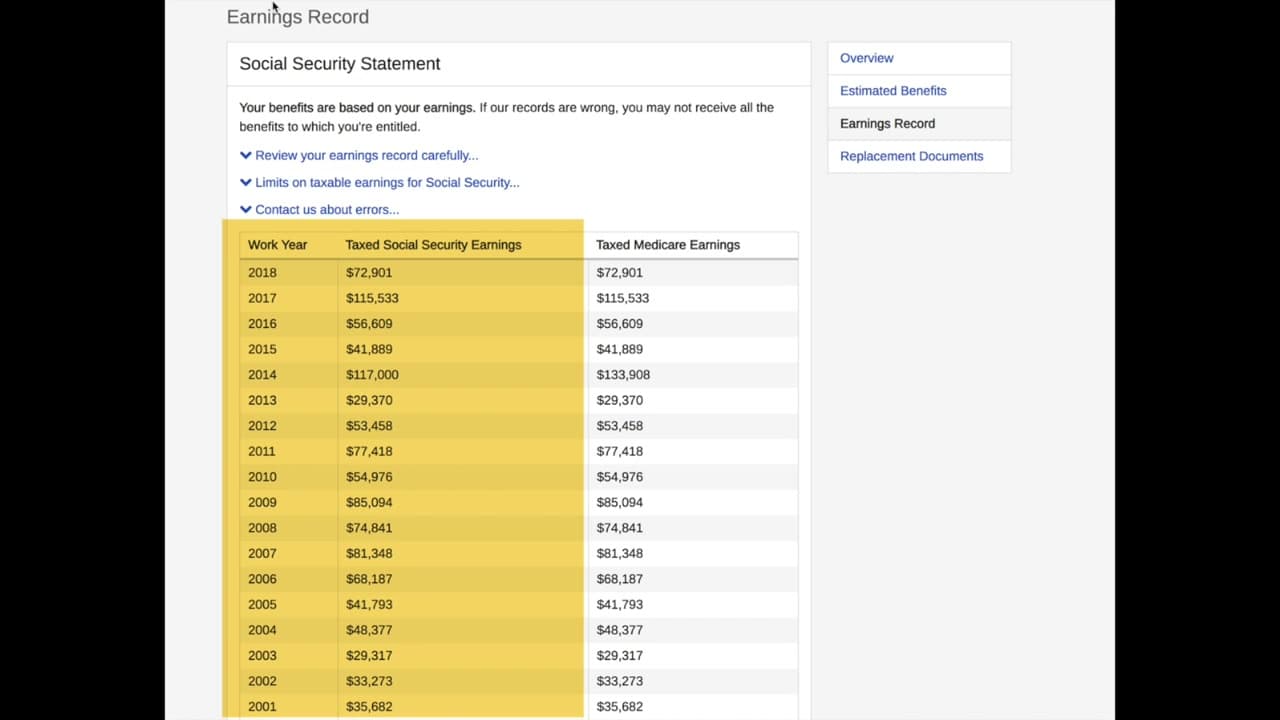

How much Social Security will you actually get? The SSA gives you a number inside your my Social Security account, but read the disclaimer right under it. It says, in plain English, we assume your earnings will continue at the same level until your retirement age, and if they are different your benefit will not match the estimate. Watch the intro at 0:52. If you plan to retire early, drop to part-time, take a sabbatical, or close out your career with a big salary jump, the SSA estimate is built on the wrong income assumption. Knowing how to redo the math yourself takes about twenty minutes and gives you the real number under any scenario.

Tip

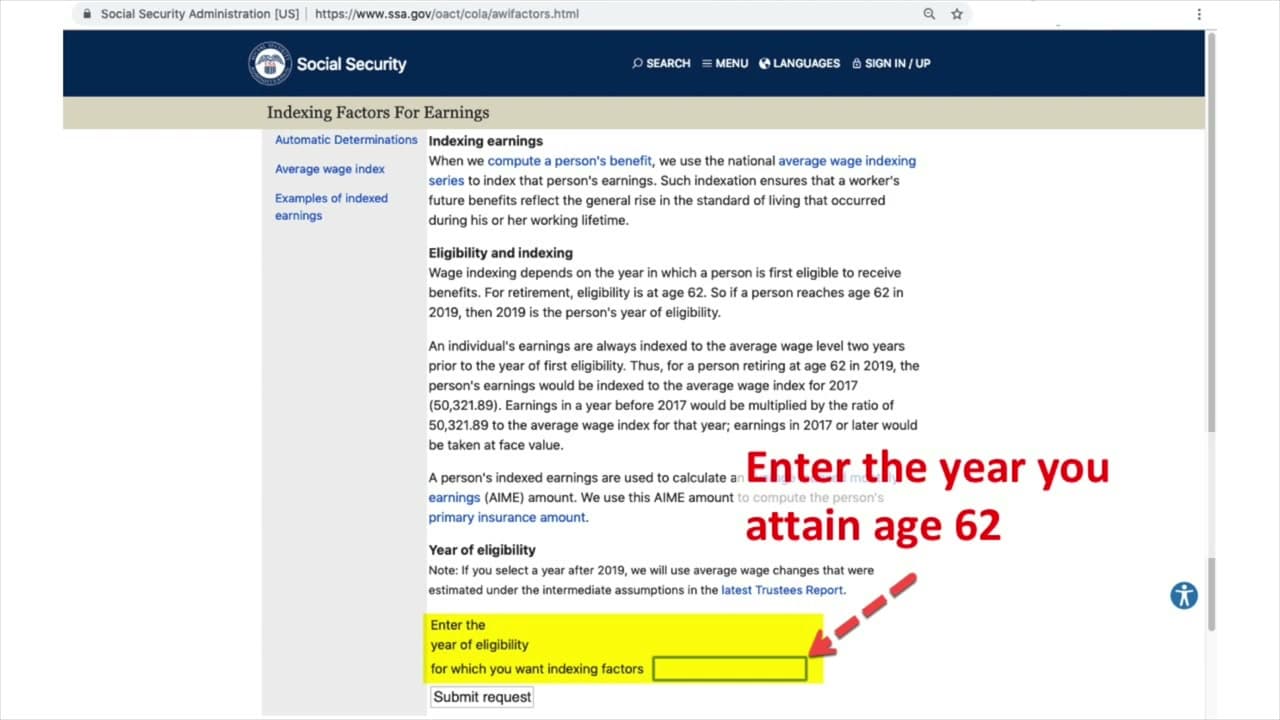

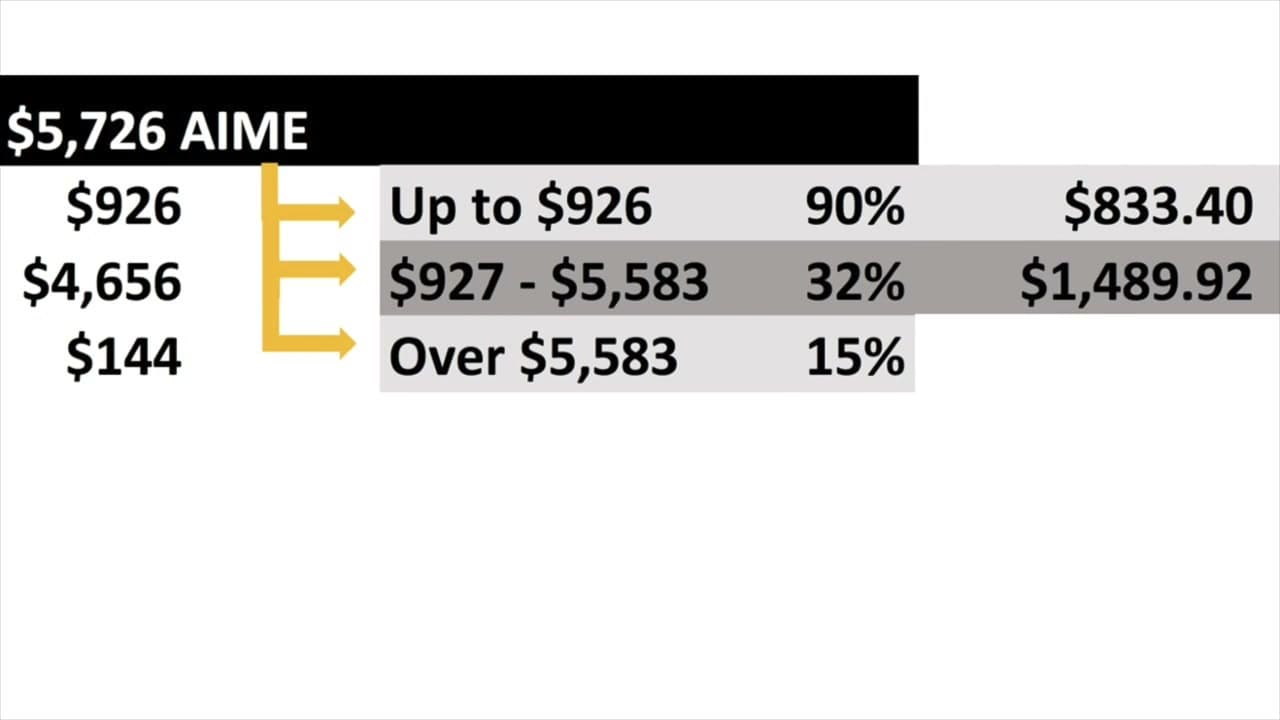

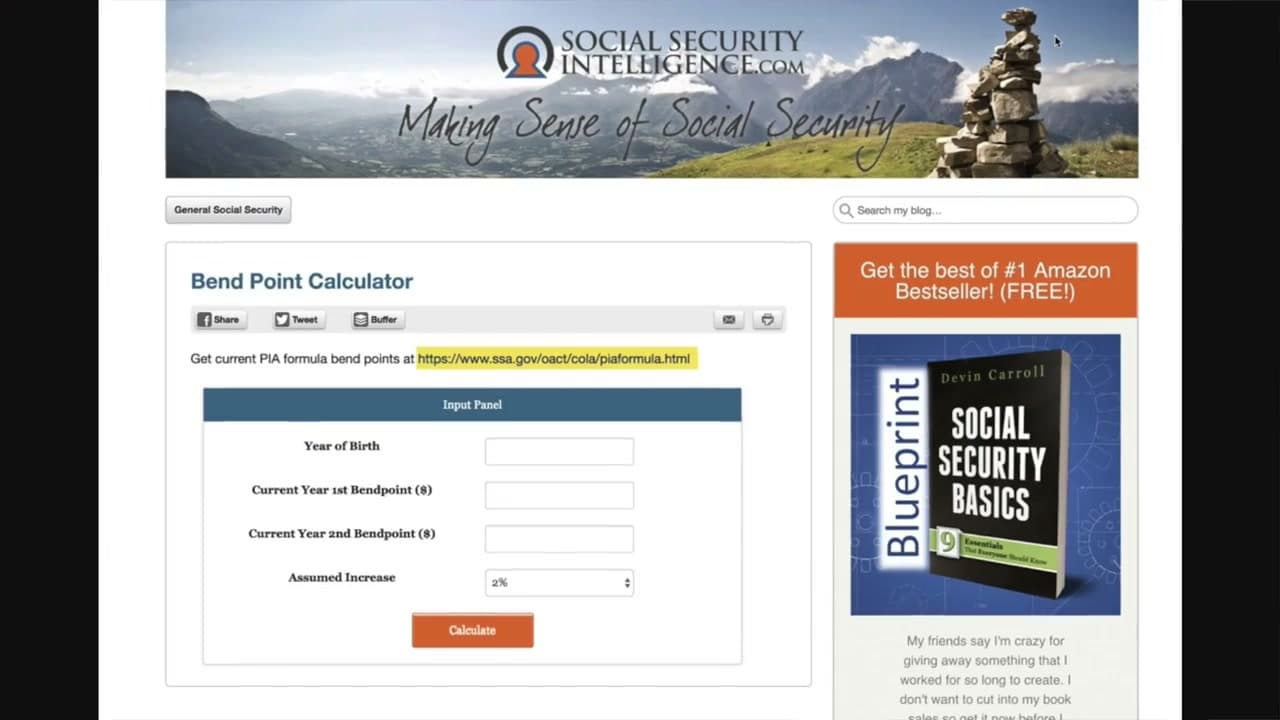

The whole calculation is just three steps: find your AIME, run it through the bend-point formula to get your PIA, then adjust for filing age. We will walk through each one.