Step 1: Confirm Whether You Have to Take an RMD This Year

0:45

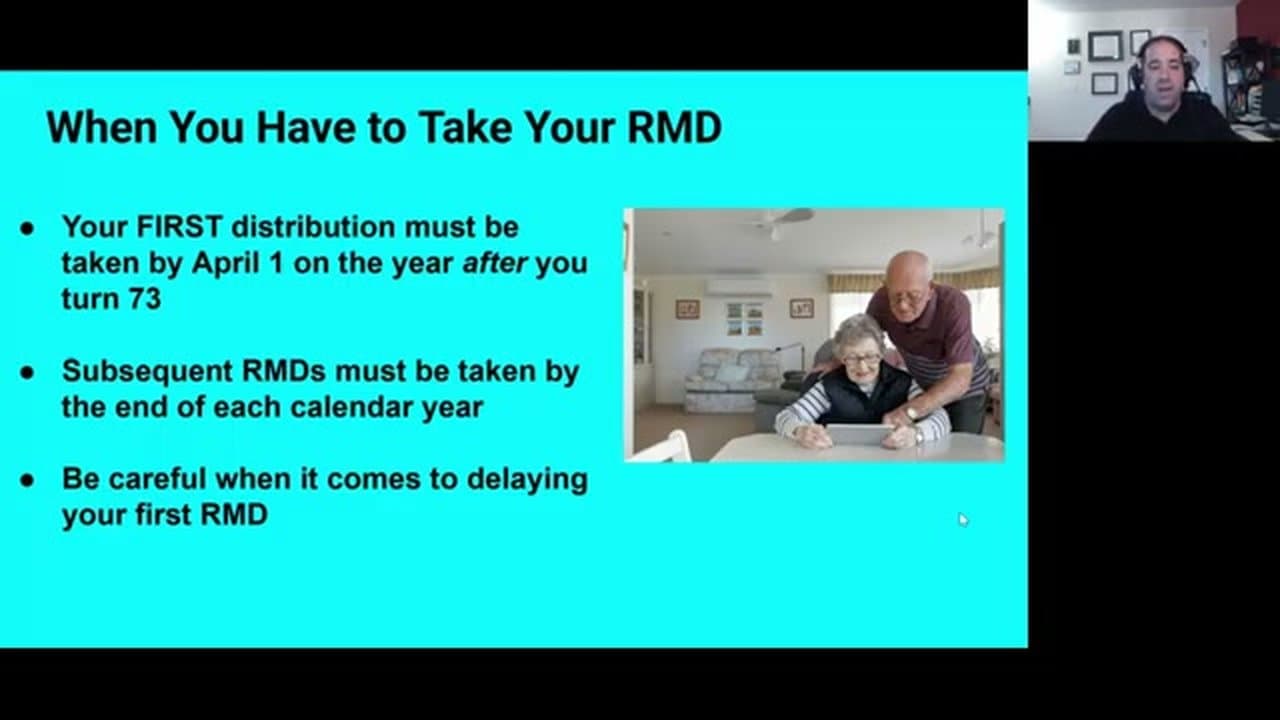

The RMD age changed under the SECURE Act 2.0. It used to be 70 1/2 for decades, but starting in 2023 the age moved to 73. So if you're 71 or 72, you do NOT have to take an RMD yet. If you turn 73 in 2025, your FIRST required minimum distribution must be taken by April 1 of the YEAR AFTER you turn 73 - that's April 1, 2026 for someone turning 73 in 2025.

Every RMD after the first must be taken by December 31 of the year you owe it. So your second RMD (the one for the year you turn 74) is due by December 31 of that same year - no April 1 grace period for subsequent RMDs.

Tip

If you're still working at age 73 and you have a 401(k) at your current employer, you may be exempt from RMDs on that specific 401(k) until you retire (the "still working" exception). It does not apply to IRAs or to 401(k)s from prior employers.