Step 1: The Two Questions That Decide If Your Benefits Are Taxed

0:30

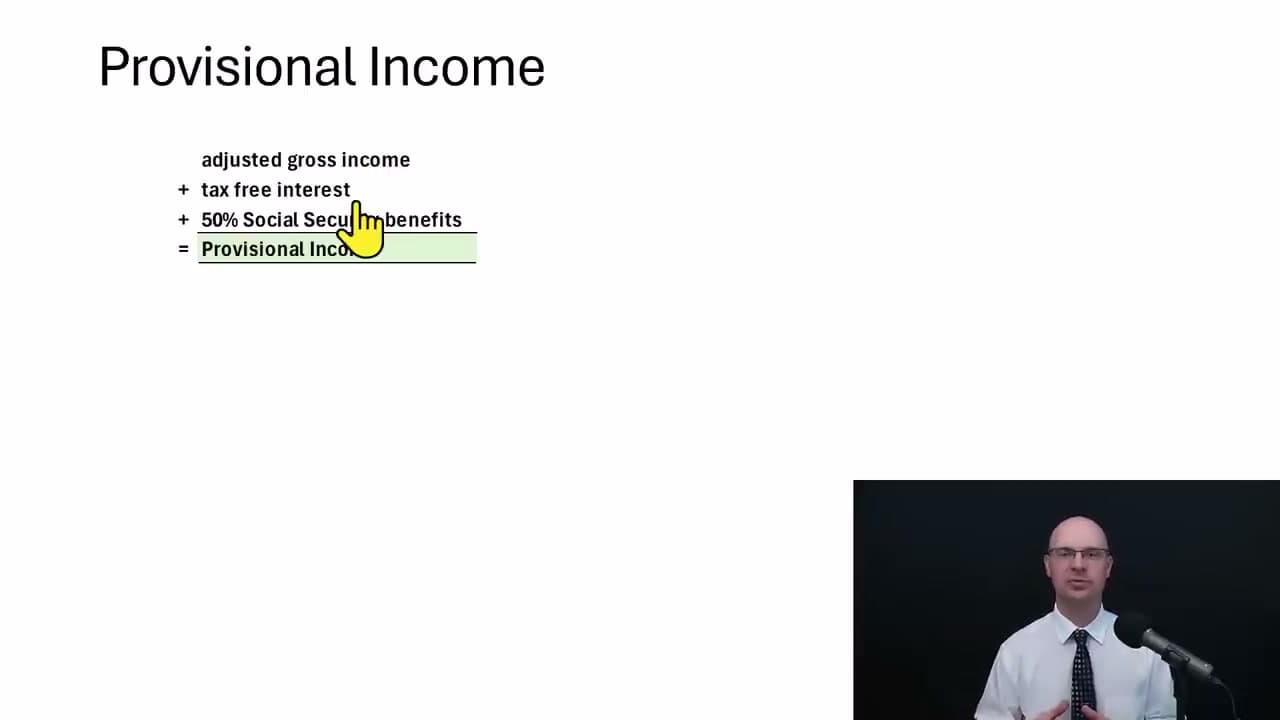

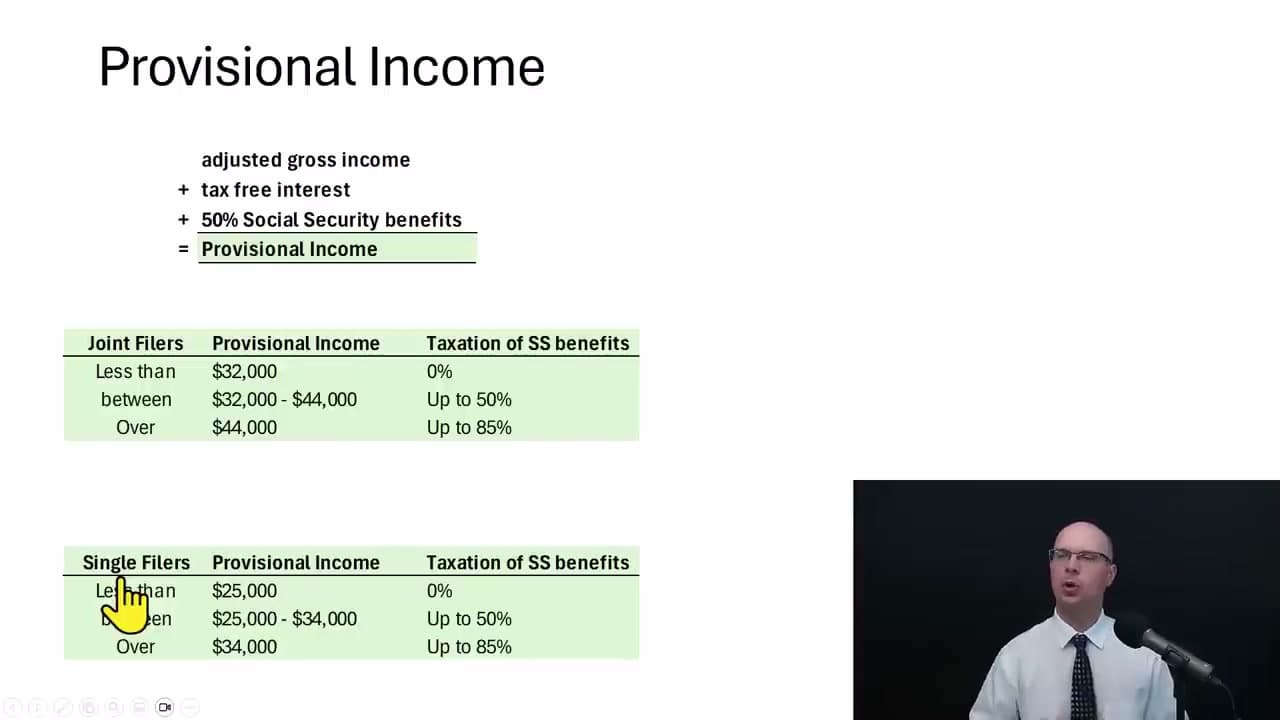

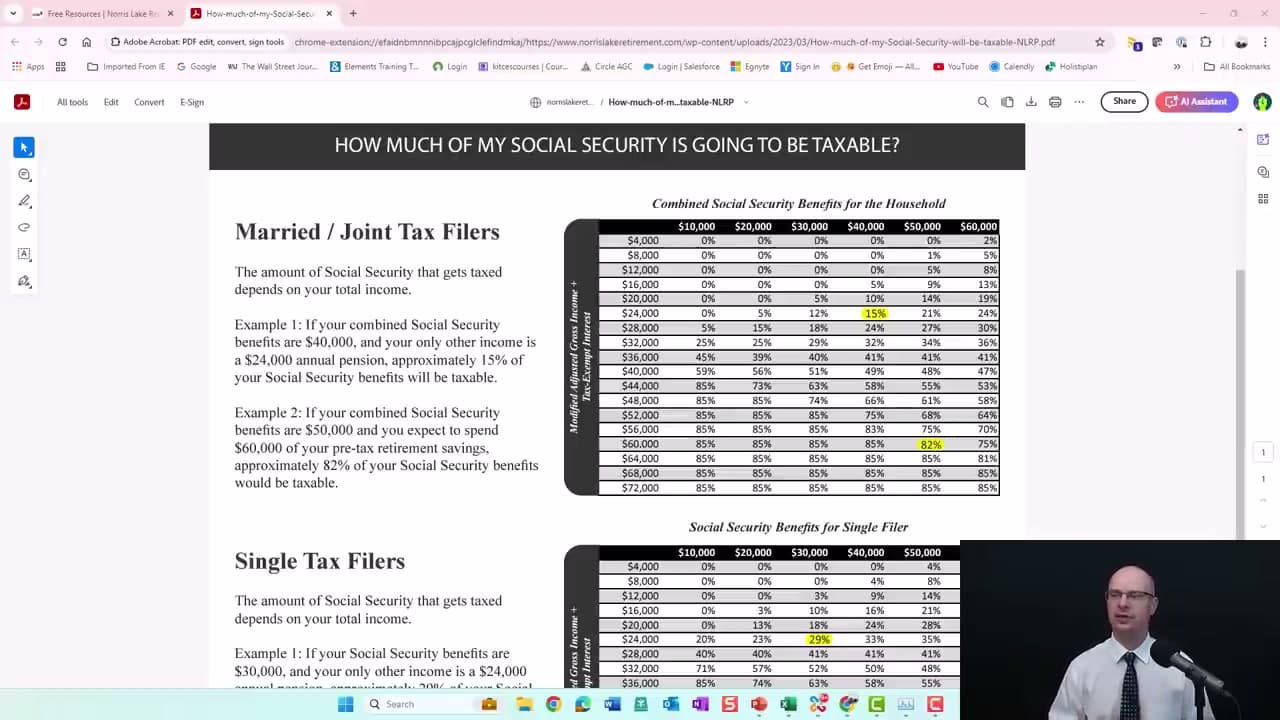

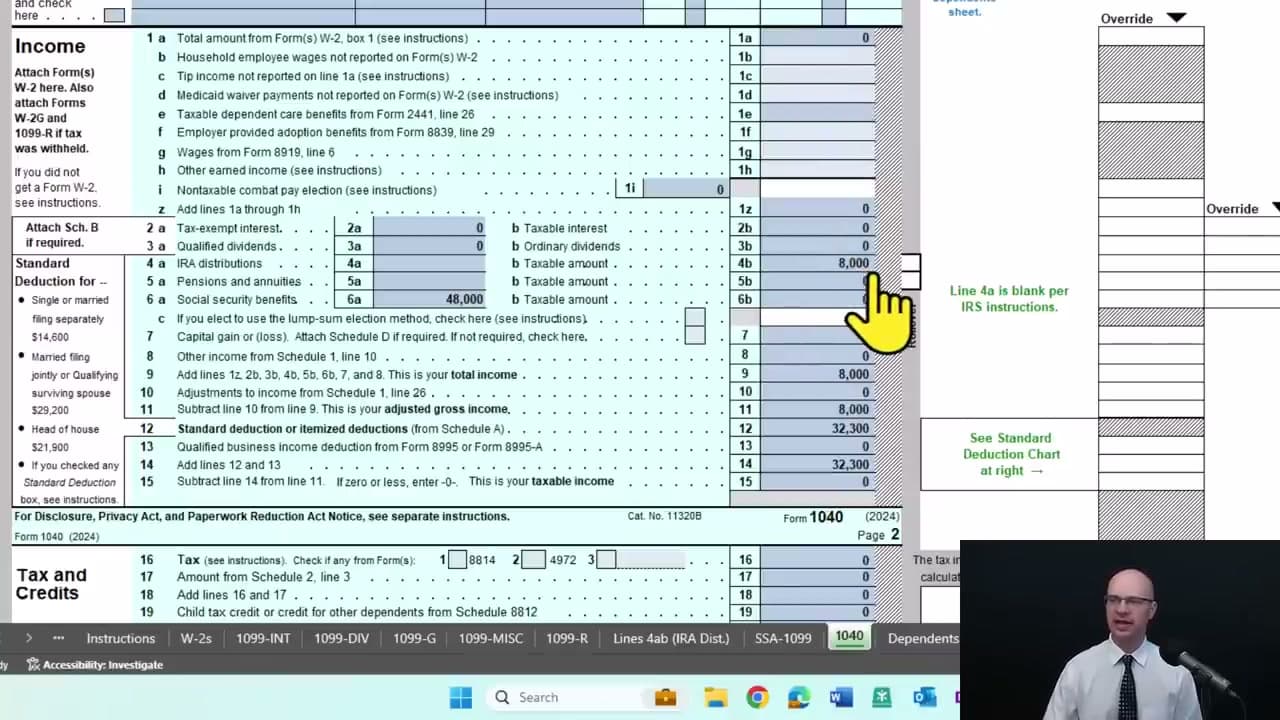

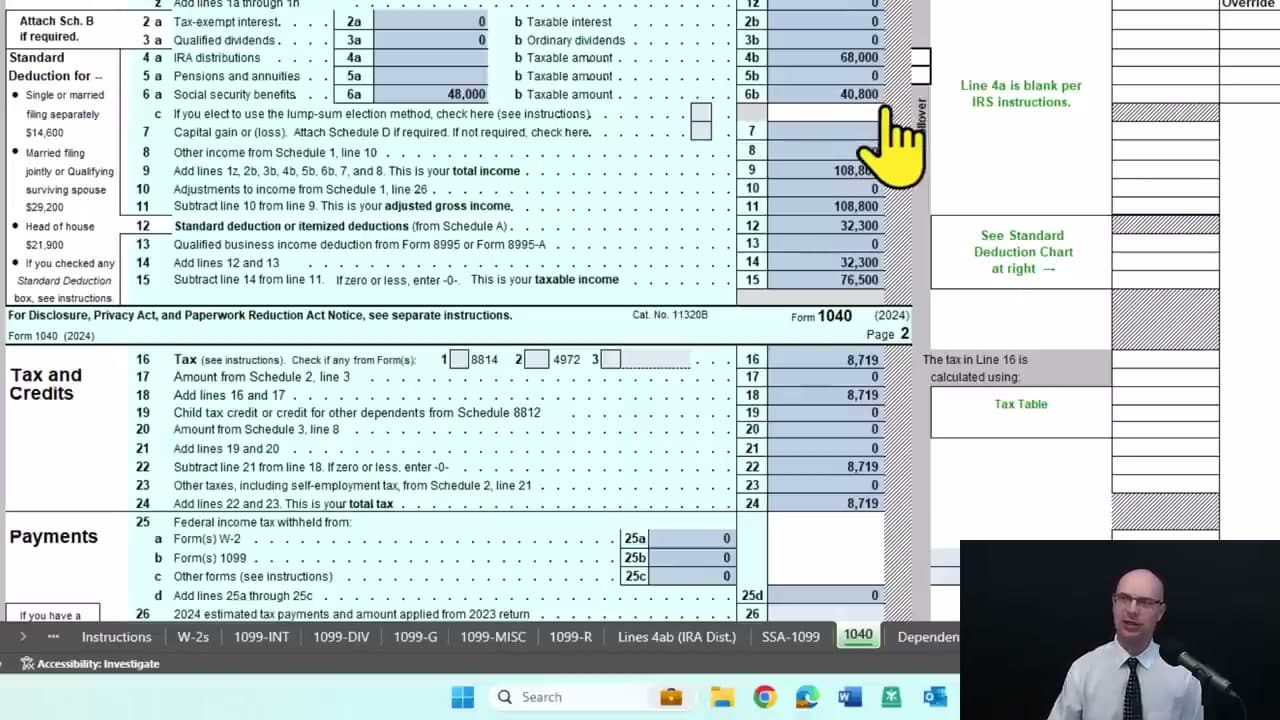

Before you panic about a tax bill on your Social Security check, you only need to answer two questions: how much Social Security did you receive this year, and how much other income did you have? Watch the intro at 0:30. Unlike a single line on your W-2, this decision rides on a small calculation the IRS calls provisional income (you may also hear it called combined income). The IRS publishes a 33-page guide on it (Publication 915), but the working idea fits on a sticky note, and we will lay it out in the next step.

Tip

If Social Security is your only income, you almost certainly owe zero federal tax on it. The taxable piece only shows up once you stack other income like a pension, IRA withdrawals, part-time work, or large investment gains on top.